Agricultural contractors (ETA – french acronym) and agricultural equipment cooperatives (CUMA – french acronym) are undoubtedly the two types of organizations most involved in agricultural equipment in the farming sector.

While CUMA are generally seen as structures for sharing and pooling agricultural equipment, ETA are more commonly regarded as structures for outsourcing, subcontracting, or delegating work. However, we will see that the boundaries between the two are sometimes blurred.

In 2025, nearly 15,000 ETAs and 10,000 CUMA cooperatives will form the fabric of this agricultural equipment ecosystem. More Specifically, a general number of structures are:

- More than 130,000 permanent and temporary employees in agricultural contracting companies (ETA); and more than 5,000 employees in agricultural equipment cooperatives (CUMA)

- More than 70% of working hours outsourced and handled via agricultural equipment by agricultural contractors; 30% by agricultural equipment cooperative

This general landscape of agricultural equipment is being reshaped against a backdrop of numerous players also seeking to find their place: cooperatives, management centers, consulting structures, etc. Among the digital tools used by agricultural contractors (ETA) and cooperative equipment associations (CUMA) are :

● Management software: work planning, real-time management of the machine fleet, invoicing management, etc.

● Connected devices: status and monitoring of machine and site operations, traceability of interventions, etc.

● Autosteering: precision of field operations, section control, and overlap management.

● On-board systems: modulation of cultivation operations

Are these digital tools within agricultural contractors and cooperative equipment associations part of a broader digitization movement in the agricultural world? I will attempt to provide some answers

More broadly, the dynamics of delegating agricultural work via agricultural equipment are changing. While the number of agricultural tasks being delegated is increasing, the complete delegation of farm operations (used by nearly 7% of French farms) seems to be stabilizing. However, the figures are not always accurate and should sometimes be taken with a grain of salt.

Are we then in the process of changing and shifting towards a new model of organization? “Delegated agriculture,” with a family farming model that is declining in favor of outsourced labor? The question is worth asking.

This report on digital tools in agricultural contractors (ETA) and cooperative equipment associations (CUMA) is also an opportunity to highlight all the knowledge that is beginning to be capitalized on the Wiki Agri Tech Platform for digital tools in agriculture. In addition to serving as a collaborative monitoring tool, this platform is now used to take a step back and look at the digital tools in place and identify trends.

As usual, for blog readers, this article is based on video interviews with industry players (whose names can be found at the end of the article), whom I would like to thank for their time . Several articles, reports, and webinars have enabled me to supplement the feedback from the interviews.

Many thanks to Geneviève Nguyen for her proofreading and comments.

Enjoy reading!

IMPORTANT PREAMBLE

I am an agronomist by training and am interested in the role of digital tools in current agricultural dynamics. In this report, we will discuss the mobilization of agricultural equipment by structures surrounding farmers: mainly CUMA (cooperative for the use of agricultural equipment) and ETA (agricultural contracting companies). There are many dynamics at work: sharing, mutual aid, pooling, delegation, subcontracting, outsourcing, etc.

Two main questions have been on my mind so far

- What digital tools are used by agricultural contractors and CUMA cooperatives?

- Does the use of digital tools by ETA/CUMA contribute to a more general movement towards more general digitization of the agricultural world?

I wonder in particular about the ability of digital tools to direct, guide, or support these different dynamics, on the one hand toward pooling, and on the other toward delegation and subcontracting. I am not seeking here to take sides on these different dynamics, especially since the boundaries are sometimes blurred, but rather to discuss what is happening before our eyes. The delegation of work remains a form of sharing agricultural equipment in the sense that the farmer has not purchased the equipment.

We will deliberately limit ourselves to agricultural equipment in this report, even though I am aware that other forms of pooling/delegation exist quite widely (in accounting, management—as in many companies in various economic sectors) and/or are beginning to appear (I discuss this briefly in this report).

I would like to point out that I write popular science articles, not scientific papers (even though I have written some in the past). Nevertheless, these articles are thoroughly researched and investigated. They are a summary (sometimes with minor revisions) of what I have read and/or heard from my interviewees. For me, popularization is not an excessive simplification of reality, but rather a way of making science more accessible. I try to make this work as objective as possible, even though I am inevitably committed to my writing.

Please keep this in mind as you read this work!

Overview of ETAs and CUMAs

A brief history is in order

Agricultural contracting companies (ETAs) emerged at the end of the second industrial revolution (around the 1880s) with the arrival of the first stationary threshing machines and mobile sawmills, mainly because the majority of farms could not afford these tools. ETA companies are therefore structures (sometimes farmers, sometimes aristocratic landowners, etc.) that take charge of this new agricultural equipment.

Cooperatives for the use of agricultural equipment (CUMA) are a little more recent, having been set up after the Second World War in 1945. They were created with a view to mutual aid and pooling resources (either as an extension of older forms of mutual aid or previous formalized organizations such as threshing unions) in order to meet the needs of small and medium-sized farms seeking to modernize. This legacy of modernization still exists today. For example, the CUMA is used by farmers seeking to process and market their products through short supply chains or to diversify their activities. For interested readers, a much more comprehensive history is available in Véronique Lucas’ thesis (Lucas, 2020).

From the 1980s onwards, the practice of delegating work via agricultural contractors began to increase significantly. Several explanations can be put forward: the downward trend in the number of family farm workers, successive reforms of the CAP, particularly those marking the shift from a logic of production support to one of risk management and relative greening of public aid, the continuous rise in the price of agricultural equipment, and various tax exemption measures for productive investments (Nguyen, 2022). Even today, some farmers want to keep their assets but no longer have the time or the means to make their equipment profitable, and therefore prefer to turn to delegated structures.

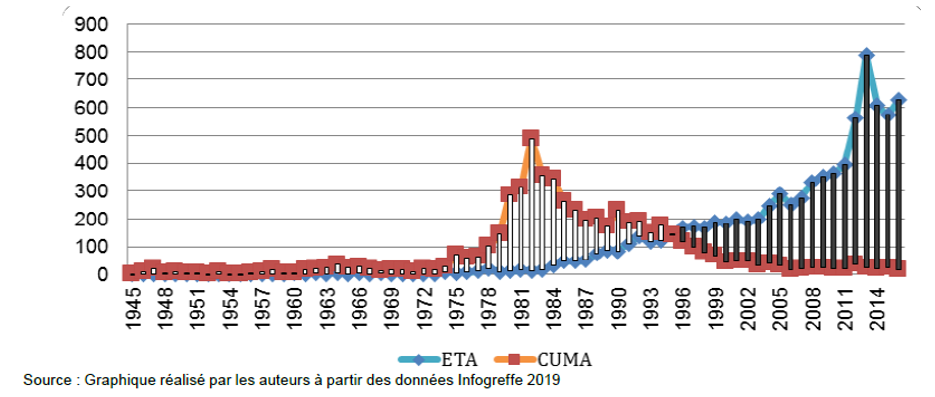

Figure 1 shows that the curves for the creation of ETA and CUMA intersect around the 1990s, marking a significant break in the logic of service between the collective and the commercial. Other phenomena may explain this dynamic: the expansion of certain CUMA at the expense of others that are dying out, and the creation of ETA solely for tax optimization purposes (we will return to this later). In this report, we will look at both the total number of these structures and the number of employees and hours worked by these employees within these structures in order to better understand this landscape.

Figure 1. Change in the number of ETA and CUMA creations. Infogreffe 2019 data. Source: Nguyen et al.,

2020

Key figures for ETAs

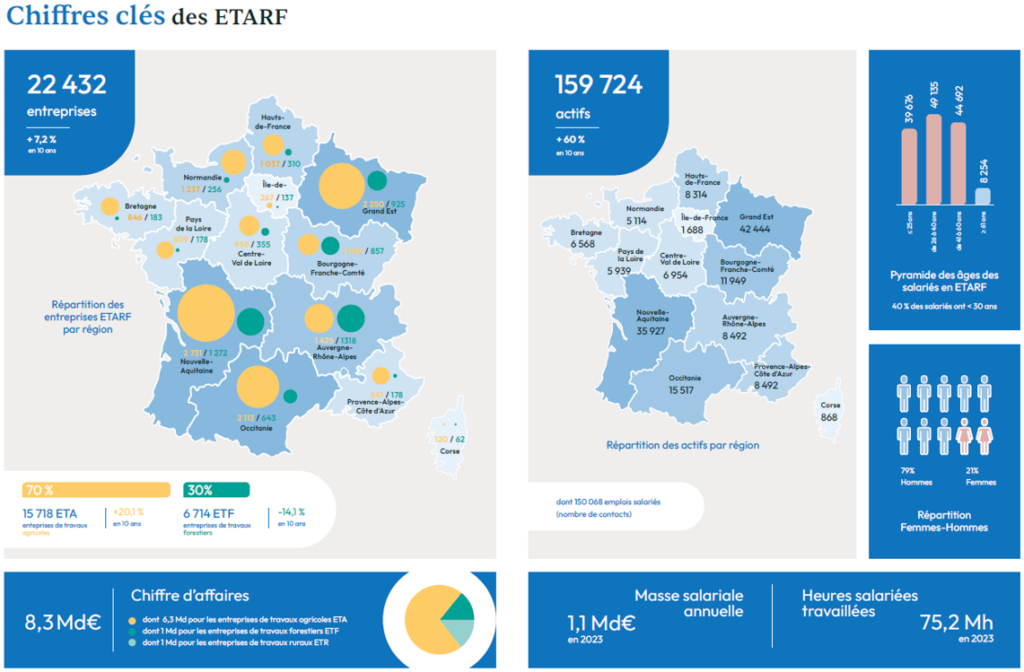

According to the latest census, there are nearly 22,000 ETARFs (french acronym) in France—agricultural, rural, and forestry work and service companies (Figure 3). These establishments are divided into nearly 15,000 agricultural work companies (ETA – those of interest to us in this report) and nearly 7,000 forestry work companies (ETF). The number of ETARFs increased by more than 7% between 2013 and 2023, an upward trend that masks significant disparities between ETAs and ETFs (+20% for ETAs, -14.4% for ETFs). Some of the ETAs (around 2,000) are affiliated with the FNEDT, the national federation of entrepreneurs of Territories. This total of 15,000 ETAs does not include the nearly 11,000 farmers who carry out custom work in their own name (Agreste, RA 2020).

ETARFs have extremely varied roles. They work with Enedis to clear power lines after storms (ETR), harvest a wide range of produce from dairy cow feed to canned and frozen vegetables (ETA), maintain roadsides (ETR), plant and replant trees in forestry operations (ETF), and more.

Figure 2. Key figures for ETARFs. Source: FNEDT 2024.

The majority of agricultural contractors (more than 80%) specialize in crop work (plowing, treatment, pruning fruit trees or vines, harvesting). Less commonly, they are used for spraying or spreading tasks, even though farmers delegate this work because they do not have up-to-date Certiphyto (individual certificate for plant protection products) certification, to avoid problems with their neighbors, or because they do not have the appropriate equipment.

Furthermore, interestingly, more than 50% of harvesting equipment is owned by agricultural contractors. The rest of the agricultural contractors focus on livestock-related work (artificial insemination, farriery and shoeing, sheep shearing, herd guarding and management, cleaning and disinfection of livestock buildings). While most agricultural contractors offer specific services, some have developed a wide range of services, from auditing agricultural properties to comprehensive farm management, including technical, administrative, and financial services. Large agricultural contractors (e.g., departmental contractors) also carry out major projects such as large-scale drainage work and large scale spreading of compost and sewage sludge.

Around 30% of agricultural contractors employ staff, and this number is increasing (by nearly 8% in 10 years). The vast majority of agricultural contractors are very small businesses (1.7 full-time equivalent on average). Agricultural contractors specializing in livestock farming employ more staff on average and have a higher wage bill than other agricultural contractors.

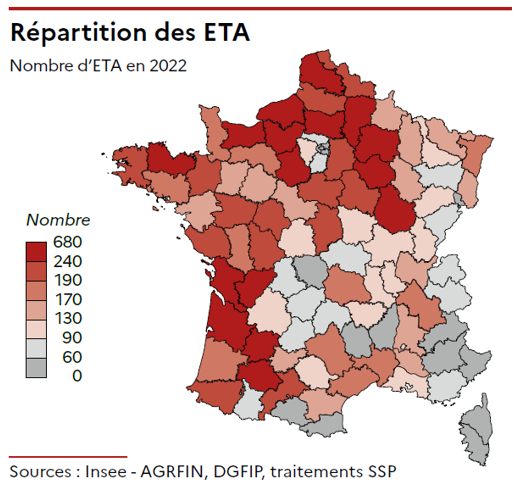

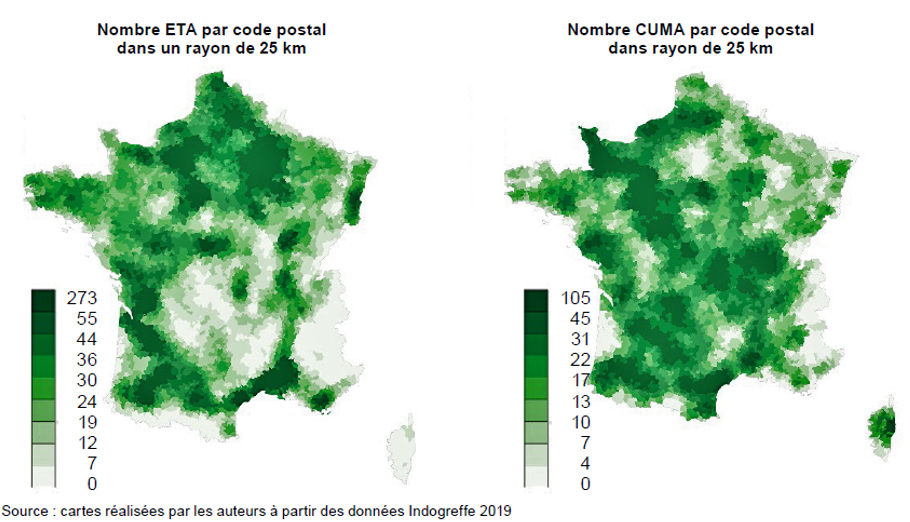

The distribution of ETAs is uneven across the country (Figure 4). Among the factors that may explain this spatial differentiation are the presence of high value-added crop sectors (e.g., sugar beet) and the size and topography of plots, which allow for greater labor productivity in northern France. In sparsely populated areas where farms are located far apart, these subcontracting structures can also act as interfaces for disseminating information and networking between scattered farms.

Agricultural contractors retain a fairly loyal customer base. Trust and geographical proximity are the two main criteria for choosing an agricultural contractor to delegate all farm work to. When subcontracting one or more tasks, farmers choose agricultural contractors based on their technical expertise and efficiency.

Figure 3. Number and distribution of agricultural contractors. Source: Agreste RA 2020.

Key figures for CUMA

Nearly 10,500 CUMA (agricultural equipment cooperatives) are located throughout France. The vast majority (more than 9,000) belong to one of the 55 departmental or regional federations of the CUMA network. This number of CUMAs, which is on a downward trend, is justified (or reassured) by the fact that the average investment and average turnover of CUMAs are themselves increasing. regional federations within the CUMA network. This number of CUMA cooperatives, which is trending downward, is justified (or reassured) by the fact that the average investment and average turnover of

CUMA cooperatives are increasing. The momentum of machinery investment is said to be higher in CUMA cooperatives than in France in general. The total machinery fleet of CUMA cooperatives is estimated at around 250,000 pieces of agricultural equipment.

These cooperatives have an average of around 20 members (the legal minimum is four). Roughly half of all farmers in France (and around one-third of farms) are members of a CUMA, sharing equipment, labor, employees, buildings, and even projects (environmental projects, energy projects, etc.).

Nearly 5,000 employees are employed by a total of around 1,500 CUMA cooperatives (15% of CUMA cooperatives are therefore employers). A tractor in a CUMA, which is often heavier and used for longer jobs on the farm, is shared by an average of 3-4 members. It can be estimated that around 10% of the total equipment fleet is in a CUMA (and therefore that 10% of the French fleet is shared).

CUMA cooperatives are owned by farmers. Therefore, there are no dividend payments. CUMA members own their agricultural equipment and therefore have every interest in not damaging or wearing it out so as not to affect their assets (my various discussions have led me to believe that, unfortunately, it is often the same members who damage the machines). Some CUMA cooperatives have had their insurance policies canceled due to excessive claims.

CUMA mainly provides shared equipment for harvesting, tillage, fertilization, transport and handling, and even space maintenance (FNCUMA, 2025). There are also specialized CUMA cooperatives with atypical equipment: sorting and seeds, composting, silage removal, wood energy (chippers, log splitters, etc.). The “CAMACUMA” agricultural equipment purchasing center helps optimize CUMA investments.

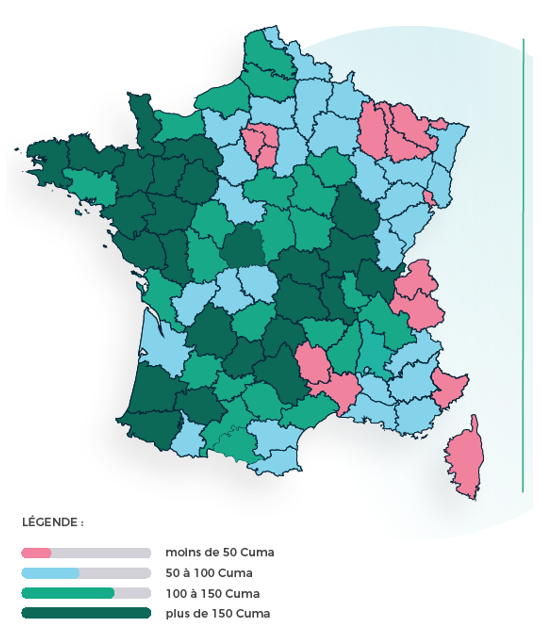

As with ETAs, the spatial distribution of CUMA cooperatives across France is uneven (Figures 4 and 5). For example, CUMA cooperatives are more prevalent in regions where dairy farming is based on mixed farming, where material investments are higher (dynamics of both crop and livestock farming). CUMA are supported to varying degrees at the political level depending on the region.

Figure 4. Spatial distribution of CUMA cooperatives across the country Source: FNCUMA 2025.

Figure 5. Number of ETAs and CUMA per postal code and within a 25 km radius Source: Nguyen et al.,

(2020). Infogreffe 2019 data

Forms and organizations of ETAs and CUMA

There are some differences between ETAs and CUMA, mainly because ETAs criticize CUMA for not being treated the same way as them. For example, CUMA are recognized as “employer groups,” which allows them to provide employees to their CUMA members.

Within this CUMA employer group (EG), hired employees divide their time between working as “employees without machinery” (working directly for EG farmers with their own machinery) and “employees with machinery” (working for EG farmers with CUMA machinery). CUMA can also hire anemployee to operate machinery and offer comprehensive services to its members without going through the employer group.

Since early 2025, CUMA cooperatives have also been exempt from TO-DE employer contributions (exemptions for the employment of casual workers and job seekers). ETA cooperatives would be excluded on the grounds that their activities are not seasonal. It should be added that ETA cooperatives are governed by the Commercial Code and not the Rural Code, and would therefore have slightly more accountability. Given the arrangements that would need to be put in place if ETA employees wanted to work for different legal entities, it seems difficult to imagine that CUMA cooperatives could simply delegate work to other CUMA cooperatives.

Despite everything, ETAs and CUMAs are not monolithic entities. Labor circulates between these structures, which also share many practices and skills. There are also a whole range of possible combinations (the CUMA for silage harvesting and the ETA for another operation). These structures therefore sometimes work together in their activities. In France, one interviewee told me that competition between ETAs in France was much less intense than in Belgium, where delegation structures hire communication agencies and do not hesitate to spend money on digital marketing.

There is no default form of CUMA and ETA. The reality is much more multifaceted.

The majority of ETAs are certainly created by farmers, even if other entrepreneurs (without agricultural operations) have also created their own. Both categories are involved in agricultural activities. Their managers and employees are required to be affiliated with the Agricultural social mutual insurance.

There are certainly some large agricultural contractors dedicated to heavy work such as spreading compost or other tasks, but the majority of agricultural contractors are farmers who have diversified their activities by adding the delegation of work to neighbors.

Some agricultural contractors are referred to as “tax contractors” in the sense that these structures have been set up to provide tax relief on agricultural machinery or tools, particularly for the benefit of farmers who consider themselves to be the contractors’ own customers. In other words, the contractor houses the equipment and possibly the hired labor, then invoices the farm to which it is attached for its services.

From farm manager and service provider in their own name, the farmer then becomes the owner of an agricultural contracting company. However, the two legal entities, the farm and the ETA, remain inextricably linked both functionally and financially, since the same person makes the decisions (Nguyen et al., 2022). There are also hybrid agricultural contractors – those that are tax-based but also carry out work for other farmers.

Some farmers carry out a few diversification activities on the margins—around a threshold of tolerance accepted by the administration—and therefore do not officially register as agricultural contractors (this is the case for nearly 11,000 farmers [Agreste, RA2020]). This contract work tends to continue over time, and the number of farmers carrying out this type of diversification (without ETA) remains in the majority. These farmers seek to monetize their skills (agronomic expertise, mastery of new embedded technologies, collection and marketing capabilities).

Some agricultural contractors may take the form of more comprehensive arrangements (such as management companies—INVIVO, for example, launched the “Sowfields” structure to provide management services) or independent managers (a kind of crop manager who manages work schedules and delegates them to other agricultural contractors). François Purseigle and Geneviève Nguyen refer to them as assistant project managers or project owners rather than traditional agricultural contractors.

Some agricultural contractors work directly for industrial companies (beets, potatoes, beans, etc.), with the packaging plant coordinating the work delegated to the contractor. Some contractors operate almost exclusively on behalf of entities belonging to a parent holding company (made up of agricultural businesses of various types) that use this legal structure to house a large fleet of equipment.

Some CUMA cooperatives can also take the form of agricultural contractors. These CUMA cooperatives are set up to meet tax challenges (like tax contractors) with one majority farmer and other smaller farmers to set up the system and comply with legal obligations. CUMA cooperatives are beginning to promote forms of delegated work among their members (via CUMA employees or other member farmers). Some very complex forms of operation exist, with a stack of SCEA/EARLs (examples of french legal forms) and a CUMA in the middle, all belonging to the same family. The CUMA is thus part of the agricultural enterprise.

The cost of agricultural equipment in France

Agricultural equipment costs weigh heavily on the financial balance sheets of farms. They represent on average 25% of total farm expenses, and can rise to 30% % depending on the sector (FNCUMA, 2024). The differences between technical and economic guidance (between a market gardening workshop and a dairy cattle workshop, for example) and even intra-technical and economic guidance (between a small and a large market gardener) can be particularly marked. It should be noted that fixed assets in equipment are limited by the growing use of third-party services such as CUMA and ETA (see the following sections on the difficulty of stabilizing statistics).

The situation is similar for delegation structures. Although ETARFs represent only 3% of customers in terms of numbers, they alone account for 30% of agricultural equipment sales. ETARFs consume 30% of agricultural non-road diesel (which represents 15% of their costs). These structures have every interest in maintaining the tax exemption on non-road diesel because these costs are significant for them.

Farmers are not really helped to reduce this expense. Farmers are often advised or encouraged to invest in agricultural machinery when they make money, which is a roundabout way of avoiding or reducing MSA (agricultural social security) contributions and taxes, with the added risk to their retirement. And this advice is not always sound, because France continues to lose its expertise in agricultural machinery consulting.

The agricultural tax system also encourages the regular renewal of machinery and the race for gigantism with the purchase of larger equipment (and therefore also larger tractors if heavier agricultural equipment needs to be towed) and therefore more expensive. Almost always new purchases, because that is what subsidies encourage… For the FNCUMA (national federation of CUMA), the conclusion is clear: one-third of the agricultural equipment purchased is superfluous (FNCUMA, 2024). Hence the interest in mutualization and delegation structures to also reinforce the versatility of shared equipment in order to lighten the burden of investment.

In addition, the price of machinery (inputs in the broad sense and agricultural commodities) has skyrocketed inrecent years (by several tens of percent, although prices appear to be stabilizing in 2025. This increase is mainly due to higher raw material and energy prices, compliance with standards, and labor costs. Inflation affects the purchase price of machinery, but also spare parts, repairs, and insurance. Some agricultural machinery manufacturers have also taken advantage of this by increasing their profit margins (sometimes only on agricultural machinery and not on landscaping equipment, oops).

This increase in the cost of machinery also places subcontractors and agricultural contractors in a difficult economic position, as they must increase their respective investments without necessarily being able to pass on the cost to their customers, at the risk of losing business. The replacement of machinery by these subcontracting structures may also be delayed when agricultural yields are lower, as this results in a poorer alignment between the cost of the machinery and the expected yields. Some therefore take the opportunity to review their machine maintenance modules (wear and tear of parts by equipment and according to the number of hours of use, preparation of maintenance schedules in accordance with manufacturers’ recommendations, etc.), even if it is not always easy to know who is responsible for maintenance and how long the equipment has actually been in use in certain mutual structures (CUMA, ETA, etc.).

The Axema 2023 economic report estimates investment in agricultural equipment at €7.25 billion. In France, by comparison, investment in CUMA (agricultural equipment cooperatives) over the same period reached €522 million. This order of magnitude difference does not therefore point towards a shift away from private ownership towards other agricultural equipment strategies: pooling of machinery, delegation of work, mutual assistance, or even co-ownership of equipment. This is also the message conveyed by the FNCUMA in its 2024 advocacy for more responsible mechanization and to combat overequipment, with farmers still too focused on high-end and premium equipment.

From a purely economic point of view, the number of agricultural machines sitting idle in barns gives pause for thought. As a reminder, the total number of agricultural machines in France is estimated at 1.5 million – compared to the number of farms: 400,000 (Source: AXEMA). This is clearly more than the total number of French trucks used for logistics and freight transport. However, the nominal utilization rate of the machines should not be very difficult to measure and could be compared to the maximum power of the machines. Due to their size, mutualization or delegation structures necessarily have lower production costs: the machines operate under optimal (or at least better) conditions, there is less downtime, and operators are better trained in the ranges of use of the equipment.

Figure 6. Eight figures providing an overview of the state of agricultural mechanization in France. Source: FNCUMA 2024.

However, the costs of machinery must be calculated correctly, taking into account downtime, time spent on the road, and equipment maintenance. Some farmers rent their machines by the hour from a dealership that has bought their old tractor from them, giving them the impression that renting ischeaper.

Several members of parliament are strongly opposed to subsidies for agricultural equipment, which they believe encourage over-equipment, and are asking the margin observatory to look into the price of agricultural equipment. According to them, these subsidies ultimately benefit manufacturers (often outside France) more than farmers themselves (since farmers buy their machines from manufacturers). This aid and/or subsidies can support initial investments in equipment and/or renewals – and very little at present for usage (we will come back to this later). It is difficult to know whether subsidized equipment purchases are in addition to or replace the planned expenditure of farms, agricultural contractors, or cooperatives.

Towards ever greater delegation of work?

While the pooling of agricultural equipment still has considerable room for growth (10% of machines are pooled according to FNCUMA 2024), practices involving delegation, outsourcing, and subcontracting seemto be attracting more interest (statistics to follow in the next section). I would like to emphasize here that these forms of delegation are currently more common among agricultural contractors. Only a minority of CUMA cooperatives are currently developing advanced delegation services (with a salaried driver operating the CUMA’s machinery), even though the boundaries are becoming increasingly blurred.

The delegation of work can be partial (for specific tasks, mainly related to cropping systems) or total (sometimes referred to as “delegation from A to Z”), with partial to total separation of ownership and management rights. However, agricultural subcontracting, and in particular the complete delegation of activities, remains poorly documented.

Geneviève Nguyen and her colleagues distinguish between full delegation “by abandonment” and full delegation “by refocusing.” In the first form of delegation, it should be understood that the farmer no longer carries out any agricultural activity. The delegation structure therefore takes care of almost all operations, including the administrative and economic management of the farm.

In the form of delegation through refocusing, the idea is rather to entrust part of the agricultural work (the least strategic, the most labor-intensive, etc.) to a delegation company so that farmers can optimize their work schedule and streamline the distribution of tasks, keeping those they are most skilled at and outsourcing the others. For example, mixed crop and livestock farmers entrust the management and operation of their crop production to a delegation company so that they can focus more on livestock farming activities.

Between 2000 and 2016, the number of farms that made significant use of subcontracting doubled, mainly among medium-sized and large farms, which also indicates that outsourcing is increasingly a business strategy rather than a solution to a lack of capacity.

Paradoxically, or perhaps in co-evolution, we still see that some large farms are equipping themselves to be self-sufficient and do not necessarily outsource work. This allows these types of farmers to work on the farm when they are available without having to fit into a CUMA schedule or an ETA slot. It should be noted, however, that owning equipment does not prevent subcontracting, for example to carry out several projects at the same time on several plots of land that are far apart (as is often the case on large farms specializing in field crops).

Even though more and more medium-sized and large farms are outsourcing services, it would be premature to conclude that small farms do not do so. The complete outsourcing of small farms is a longer-standing phenomenon, with non-farmers sometimes becoming owners of small structures as a result of successive inheritances. Alongside this phenomenon, small farms that used to outsource have been bought out by larger farms (due to retirement). Others have turned to forms of service provision that are more difficult to identify and quantify: recourse to neighboring farmers, comprehensive farm equipment rental services.

In 2020, nearly one million people reported working on a farm under an employment contract – across all regions and types of production (with a slightly higher concentration in certain areas: market gardening, arboriculture, cereals). Of this million employees, nearly 235,000 are no longer directly employed by farms (this figure stood at 80,000 in 2003). Outsourced employees thus provide an increasing number of declared working hours. Outsourcing takes many forms: the use of temporary employment agencies, French service providers (agricultural contractors, ETA) or foreign service providers (posted workers), agricultural equipment cooperatives (Cuma) or employer groups (GE) [Magnan & Laurent, 2025]. We will return to this broad landscape of delegation in the following section.

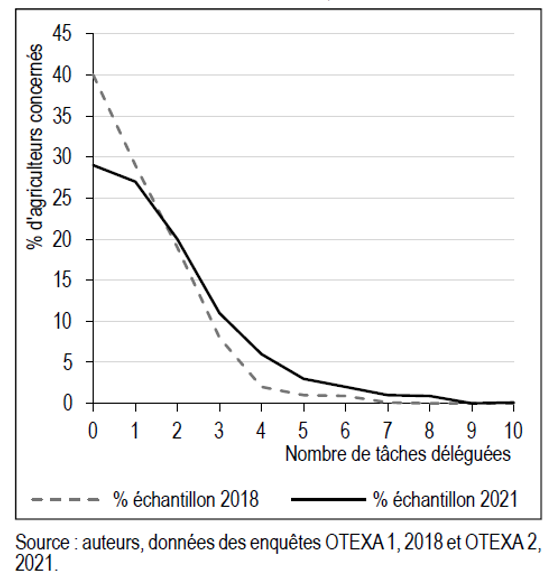

Figure 7. Proportion of farmers outsourcing according to the number of tasks delegated in southwestern France between 2018 and 2021. Source: Nguyen et al., 2022

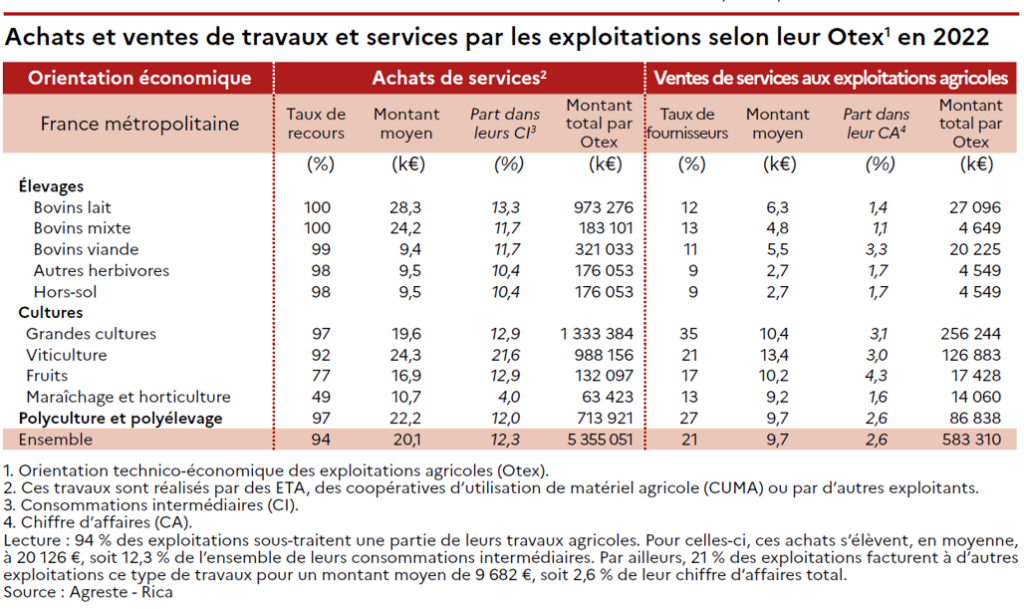

The importance of subcontracting also depends on the type of production. Almost all livestock and arable farms, as well as nearly 8 out of 10 arborists and 1 out of 2 market gardeners, use work delegation structures (see Table 1). It is understandable to prefer delegating work to pooling equipment (e.g., in a CUMA). If equipment has to be shared with farmers who may have the same needs at the same time (because they use similar technical methods within a CUMA), and if this is compounded by increasingly limited windows of opportunity for action, it is essential to be particularly well organized. Some farmers will therefore prefer to contract with an agricultural contractor (ETA) or another form of subcontractor.

Table 1. Purchases and sales of work and services by farms according to their OTEX in 2022. Source: Agreste, RA 2020

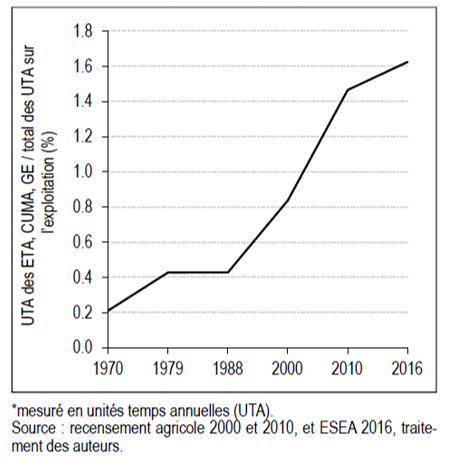

Not only are more farmers outsourcing, but they are also outsourcing more and more tasks. Although this external labor force accounts for only 4% of the work input on farms, the corresponding volume of work (in annual time units or ATUs) has almost quadrupled (Figure 8), rising from 8,000 to 29,760 AWUs between 2010 and 2016, through agricultural subcontracting companies (ETAs), agricultural equipment cooperatives (CUMAs), and employer groups (GEs). The value of agricultural services, which mainly concerns agricultural work, has also increased significantly. In a 2022 article, the media outlet Entraid highlighted that the use of service providers to carry out crop work had increased significantly between 2010 and 2020: +26% for CUMA and +39% for ETA.

Figure 8. Change in the share of the volume of work (measured in annual time units, ATU) provided by ETAs, CUMA cooperatives, and employer groups in relation to the total volume of work on the farm (in %). Source: Nguyen et al., 2022

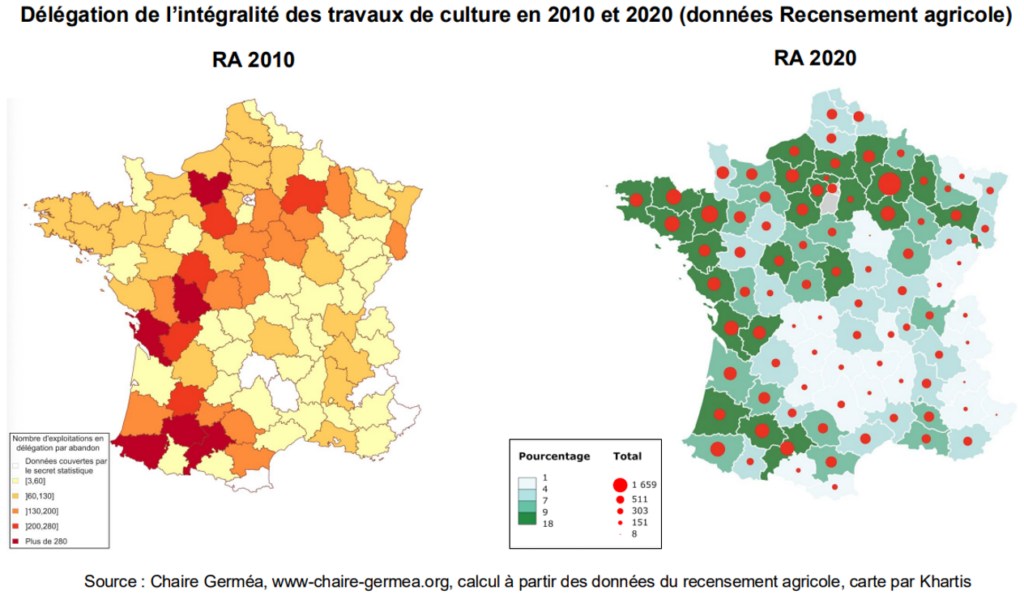

Approximately 7% of French farms have outsourced all of their agricultural activities (Nguyen – LinkedIn publication 2025). The complete outsourcing of work in farming systems appears to be stable across France, but hides different realities when looked at more closely. Full outsourcing appears to be increasing in certain regions (West, Center-North, Grand Est), particularly the most specialized ones, for different reasons (refocusing on livestock farming for some, asset management for others). It would be interesting to see if there are any correlations with major market trends such as the dynamics surrounding the carbon market.

Figure 9. Number of farms with full delegation of their work. Please note that the 2010-2020 period does not yet reflect double-digit inflation in agricultural equipment. Source: Nguyen 2025 – LinkedIn

Internationally, the outsourcing of work is sometimes much more prevalent than in France (Reardon et al., 2024). In Myanmar and Indonesia, large agricultural supply companies have their own fleets of equipment and take charge of outsourcing work. In the United States, services are developing to install plant cover on farms and thus sell carbon credits. And it is perhaps in China that subcontracting is developing particularly rapidly, notably because farmers are leaving to work in cities because their land isno longer sufficient to support them.

Why do farmers outsource part of their agricultural work? Geneviève Nguyen and her colleagues distinguish between several types of farmers who use outsourcing:

- Profile 1: farmers, mostly young, under the age of 50, who have set up their farms as their main activity and wishing to refocus on their core business and production

- Profile 2: farmers who run medium-sized to large farms, aged over 50, retired (or close to retirement) with no immediate successors, who do not wish to lease their farms due to the status being considered too restrictive and prefer to delegate to an agricultural contractor while awaiting a hypothetical takeover or even a future sale.

- Profile 3: multi-activity farmers of all ages who do not have the time and, like the first profile, prefer to subcontract rather than hire a manager—for cost reasons, which include salary but also other transaction costs (searching for employees, supervising work, and managing potential conflicts)—but also to avoid investing in equipment

Perhaps more or less intertwined within these profiles, some farmers subcontract to test a machine, outsource risks (spraying, investment), access precision machinery, or because they experience a high accident rate on their farm (machine breakdowns, disease, etc.).

With its many different roles, the farming profession requires a fairly broad range of skills. And we may wonder whether the management of agricultural equipment and the operation of machinery is a task that will continue to be carried out by the farmer himself or whether he will prefer to delegate (sacrifice?) this section to ancillary companies (whether or not through an agricultural contractor, and whether the machines are autonomous, robotized, or not). It remains to be seen whether, in addition to agricultural equipment, the use of subcontractors will increase for administrative tasks, particularly in relation to CAP declarations and tax returns, but also for advisory services: agronomic, legal, or even asset management.

The financial costs of agricultural equipment are significant for farms (see previous section), and many farmers are no longer willing to make such investments. Investing in new assets for a farm raises questions about fluctuations in agricultural income and the price of machinery in the broad sense (machines, spare parts, etc.). The contracting company then becomes the entity responsible for equipment breakdowns, resource allocation, and equipment management. From a financial standpoint, outsourcing is also a way to test an expensive machine before potentially investing in it. Indirectly, outsourcing is also sometimes an alternative to over-equipment, whether on the farm or collectively (for example, if a CUMA makes significant investments in equipment).

Among other things, the cost of agricultural equipment is a barrier to young farmers setting up their own farms. Using an ETA is therefore a way for new farmers to delay and thus secure recruitment and payroll costs. The provision of services through a farm contractor or other delegated structure could also be included in the criteria for awarding the young farmer grant (DJA acronym in french) aid as a possible economic model, whether temporary or not. The use of subcontracting also makes it possible to smooth out peaks in activity (following a setback, for example) and thus reduce the intensity of work during busy periods

This outsourcing goes beyond the simple financial argument in that farmers thereby externalize the risks to their health and even the management of conflictual relations with their neighbors. Environmental standards (specifications to be met, non-treatment zones, etc.) are pushing farmers to delegate constraints that they may find difficult to meet, either because they lack the appropriate equipment or because they are not always aware of their existence. Paule Yacoub’s thesis, currently underway in 2025, seeks to understand the effect of environmental reforms (water protection, plant protection products, etc.) on the organization of work in agricultural contractors.

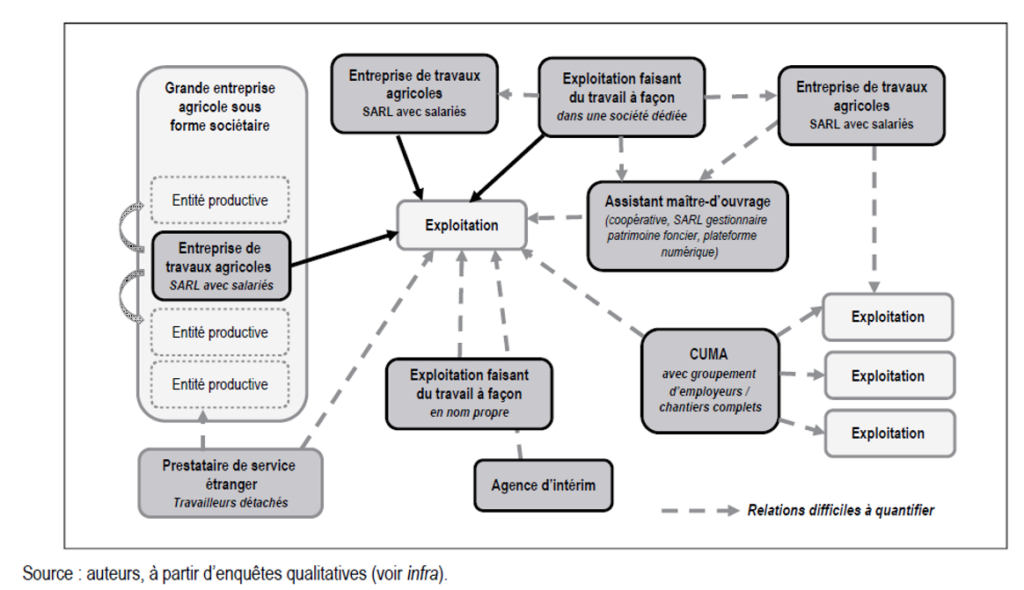

The agricultural contracting landscape is vast

The agricultural subcontracting landscape is actually much more diverse than it appears (Figure 10). Although agricultural contractors are in the majority, they have not eclipsed all other service providers. For example, there are:

- Organizations that position themselves as project management assistants, acting as intermediaries between farmer clients and agricultural contractors. These organizations do not provide the services themselves, but organize them on behalf of their clients :

- More or less informal neighborhood ties, mutual aid, and sharing arrangements between farmers: straw-manure exchanges, alfalfa harvesting by livestock farmers on the land of their arable farming neighbors. This local cooperation ensures technical dialogue and sociability between farmers.

- Farmers working on their own behalf.

- Agricultural cooperatives which, in order to cope with new forms of competition from other storage organizations and to maintain their collection capacity, may go so far as to create commercial structures and offer their clients collection management tools (management of products to be marketed, contracting of volumes with the various storage organizations, monitoring of storage and destocking, continuous monitoring of prices, access to market offers for the latter, etc.). Some cooperatives also buy back agricultural contractors through subsidiaries

- Agricultural study and technical centers (CETA) that develop a service and commercial unitsdedicated to agricultural work

- Temporary employment agencies, foreign service providers, or companies not covered by the agricultural social security system (MSA) are becoming increasingly important in certain sectors such as viticulture and arboriculture

We will discuss these different forms of subcontracting further in the rest of this report.

Figure 10. The complexity of the subcontracting landscape in French agriculture. Source: Nguyen et al., 2022

It remains difficult to obtain very precise figures.

The figures presented above should be taken with a grain of salt. In general, identifying subcontracting and delegation in agriculture remains difficult and poses a real methodological challenge (Nguyen et al.,2020; 2022). The legal definition of subcontracting is not always very clear, as shown by the example of tax-based agricultural contractors cited above. The lack of data should be viewed in parallel with the small number of studies focusing on the delegation and subcontracting of agricultural work.

The available statistical data is fragmented and heterogeneous. Among the main sources available are:

- three questions in the latest censuses and structural surveys conducted by the of the Ministry of Agriculture,

- data from INSEE,

- MSA data on labor,

- data on the creation of establishments from the Infogreffe register of commerce and industry,

- data on CUMA cooperatives from the High Council for Agricultural Cooperation (HCCA), and

- various data from professional federations s of ETA and CUMA (activity reports activity reports and key figures).

In theory, subcontracting activities cannot be carried out on a marginal basis by agricultural holdings, but only by service companies, such as agricultural contractors (ETA) or temporary employment agencies. Farmers would be allowed to carry out custom work on behalf of others in their own name. Furthermore, since 2013, the requirement for company certification for phytosanitary services means that farmers can no longer carry out this type of work in their own name and must set up a commercial company. Despite this, the rise in the price of agricultural equipment has led to an increase in inter-farm services, and not all farmers have complied with the requirement to regularize their status. The control services (Sral) acknowledge that they are unable to identify these reprehensible practices, let alone punish them.

Several other services are not (yet) considered subcontracting:

- Complete projects offered by certain CUMA cooperatives where the farmer does not carry out the work himself but entrusts it to the CUMA.

- Integration contracts between farmers, cooperatives, or agri-food industries with services included such as animal removal or building cleaning

- The tasks of seasonal workers managed by temporary employment agencies and foreign service providers (pruning, harvesting, etc. in viticulture, arboriculture, or market gardening)

Digital tools in agricultural contractors and cooperative

equipment associations

The results presented in this section are based on discussions and readings. They would need to be confirmed by quantitative surveys. It may be interesting to distinguish between sub-populations, such as agricultural contractors set up by farmers and those set up by entrepreneurs with no initial agricultural activity.

In this section, we will look at a range of digital devices that agricultural contractors and agricultural equipment cooperatives are are equipping themselves with. Adoption is not widespread and varies depending on the tools presented.

For task management and work planning software in particular, adoption seems to be more of a necessity than a choice – in response to increasingly demanding regulations and the arrival of mandatory electronic invoicing from 2026. Agricultural contractors and CUMA cooperatives are generally accustomed to their routine and the way of working they have inherited.

Agricultural contractors are increasingly investing in digital tools when they provide multi-service offerings with a fleet of several machines and employees. In these complex organizations, the sometimes very large number of plots (or micro-plots in viticulture), equipment, and/or employees (operators, drivers, etc.) to monitor requires the use of digital tools to optimize task management and improve working conditions.

CUMA cooperatives may also tend to purchase high-end equipment that is more powerful and has more features, and take advantage of the benefits of pooling resources (without necessarily all of these features being used by members). With their longer decision-making cycles than ETA cooperatives, CUMA cooperatives tend to follow natural technological developments. In CUMA cooperatives, digital services in agriculture tend to be more prevalent when one or more employees are hired and/or when certain members are leaders (often team leaders) or driving forces in this area. The advantage of CUMA cooperatives remains that these structures can bring a certain number of members behind them, investing more in digital technology than each member would have done individually.

Internal tools

I am referring here mainly to digitization tools—a way for agricultural contractors and cooperative equipment associations to move away from the traditional system of field notebooks with work orders that are usually filled out by hand. These tools are known as “ERP” (Enterprise Resource Planning) systems. There are quite a few of these management software tools available, although the level of adoption varies considerably between them.

The main ones are: Léa (Smag), Facilitime (DCD), Kropeo (Trackengo), ISA Eta (Isagri), MyCumaLink & MyCuma Planning et Travaux (FNCUMA), MyJohnDeere (John Deere), Kandorlab (formerly Portik), and Contractor (MyEasyFarm).

Like many IT tools, this management software is promoted as a way to avoid data entry errors and oversights of all kinds: errors in the work units entered, lost/forgotten/incorrectly written/inaccessible purchase orders, and time counting errors. Work sites are entered directly into databases (which can take several days with a paper format and requires re-entry later during invoicing). Work schedule management is also refined, which can save a few minutes/hours of service if these schedules are generally rounded.

Taking a step back, these management tools also serve as proof of work and therefore enable farmers to (re)gain confidence in their service providers. The contractor can thus show what has been achieved in terms of services, adjust rates according to the actual size of plots, etc. One example is the issue of plant protection products, particularly in vineyards, where customers are waiting for feedback on their phytosanitary treatment declarations (product used, quantities actually applied, date of application, weather conditions at the time of application, etc.). By computerizing this data, information becomes more symmetrical and fluid in the sense that each of the parties involved in the transaction can access it. For example, it is useful to show the actual areas worked because some agricultural stakeholders have a rather distorted view of their actual areas.

Here is a rough classification of the main uses of this management software :

Work planning:

- Activity schedule management (highly unpredictable schedules that change all the time time, particularly due to weather conditions)

The planning of agricultural contractors/cooperative equipment associations (ETA/CUMA) can be very volatile due to, among other things, changes in schedules, breakdowns, longer than expected construction sites, weather conditions, etc. It is understandable that real-time monitoring and regular updating of information on a digital tool is not easy (and even less so when it comes to making forecasts in view of this uncertainty).

The available mapping data provides access to parcel blocks, which can then be assigned to the farming operations that will be carried out on them. Often, ETA managers are familiar with the parcels they work on, and mapping tools are used to share this localized knowledge with employees.

- Employee management (updating changes to driver’s licenses, etc.)

- Employee time management: for counting and grouping hours, etc.

- Work order management: which have always been filled out by hand.

- Reservation of equipment for specific time slots

- Sharing GPS tracks

- Structuring customer relationships

Real-time management (control tower)

- Mapping of equipment in use (knowing where the equipment is, who is using it, etc.).

Equipment is often scattered among the various members of the CUMA.

- Management of the fleet of tools and machines

When the machine fleet is large, a driver/operator may be responsible for a particular machine, especially when they start to become sophisticated.

Downstream management:

- End-to-end traceability of operations (reports on work completed – time, hectares, plots worked, etc.).

It is easier to assign operations/sites to users when the parcel layout of a customer or members (of a cooperative, EARL, or other) is provided. This allows for more detailed analytics. When this is not the case, machine usage is generally assigned to the requesting structure without much detail. It should be noted that not all of these software programs are capable of handling multi-farm operations. If an operator has carried out a spraying operation on five different farms, they will have to enter this operation five times, once for each farm.

In view of rising energy costs, some subcontracting companies are cracking down on fuel waste: conditions of use of machinery, tractors idling, when machines were last refueled, etc. Some companies are starting to charge for and rationalize travel, particularly when they work in large geographical areas and tend to spend a lot of time on the road.

- Billing (allocation of expenses to reallocate costs based on contingencies, work [yield, driving hours, working hours, downtime, etc.])

Some of these tools also do not handle the “Billing” aspect, considering that this task is a job in its own right, and therefore prefer to connect to dedicated software on the market to handle customer billing.

- Complete report on equipment use: uninvoiced travel rates, mileage, cost price of a machine (based on purchase price and other factors).

It is quite rare for a farmer to ask for a maintenance invoice for a machine (if they buy it second-hand), whereas this is often something that is done when buying a car for personal use. If the traceability of the life of agricultural equipment were available, this machine would potentially be easier to resell. With the increasing cost of agricultural equipment and the challenge of spare parts (particularly for towed equipment), it is conceivable that the industry will want even more detailed traceability of their machines.

- Payment

- Reminders

We can also mention a few additional uses, mainly related to CUMA (but not exclusively):

- Identifying equipment already present in the territories,

- Connecting CUMA cooperatives and organizing equipment sharing,

- Rethinking the balance between members’ current needs and the equipment available

External tools

I am particularly interested here in digital tools embedded in agricultural equipment (positioning systems, autosteering, on-board sensors) and robotic and/or autonomous systems. As discussed previously, I would like to continue this work with in-depth surveys of usage in the field.

Within the CUMA, Nassim Hamiti, agricultural equipment project manager, took part in the exercise and proposed the following quantitative estimate (to be challenged):

● Of the approximately 6,000 tractors (new, excluding used) still in stock (unsold to date), one in three tractors is equipped or pre-equipped with autosteering equipment.

● Of the 2,879 weeders in the fleet, 6% are equipped with active autosteering.

● Of the harvesters, 8% are equipped with autosteering and/or yield sensors.

● A total of around 100 connected meters/boxes are installed in 80 equipped CUMA cooperatives

● Approximately 6% of CUMA cooperatives use “Mycuma Planning et Travaux”.

Connected boxes and meters: CUMA and ETA are equipping themselves with connected boxes and meters. And the list is quite extensive: Karnott, Aptimiz, Kemtag (Ogo), Geotrack (Isagri), Samsys, Alvie, Scopix, JD Link (John Deere), etc. These tools, which are installed directly on agricultural equipment (either connected to the CAN bus or magnetized), make it possible to track the movement of agricultural machinery: hours on the road, hours worked, and even downtime. This facilitates the work of providing proof and invoicing for agricultural projects. The precise geolocation of machines enabled by these devices makes it possible to detect errors in both location (a row or aisle that has been missed) and operation (nozzles that have not been turned back on). It also allows for optimization in terms of machine usage over time, provided that an agricultural contractor or cooperative makes the effort to analyze the usage data of their employees’ and/or members’ machines.

These tools sometimes allow you to go even further: automatic detection of cultivation operations, machine data feedback (by connecting to the CAN bus, etc.). As part of the digitized phytosanitary register scheduled for early 2027 (initially planned for early 2026 but postponed by one year), it is conceivable that devices could be used to report the number of liters of phytosanitary products sprayed per plot and at each location within the plot, or even to determine whether equipment has been used on a plot and under what operating conditions. However, these devices do not have access to all the information associated with the work in progress. The interaction between these devices and the ERP (entreprise resource planning) tools mentioned above therefore raises questions. We will have the opportunity to discuss this further.

In addition to the purchase and subscription costs, membership of these boxes is closely linked to the employee factor of the CUMA or ETA. Quite simply because it is often the employee who will deploy these boxes within the structure: managing data feedback, loading meters, explaining on which machines the boxes have been installed, etc. Some interviewees told me that when installing the boxes, the CUMA generally charges members a little more, as they tend to underreport the hours and/or hectares worked—whether voluntarily (for example, because members do a little subcontracting on the side) or not (forgetfulness, guessing, etc.).

Autosteering & Geopositioning: The majority of agricultural contractors and cooperative equipment associations (ETAs and CUMA) are investing in autosteering equipment (mostly autosteering rather than more precise geopositioning tools such as RTK – real time kinematic), especially the larger ETA and CUMA. Those who have invested rarely go back. The question no longer really arises when renewing machinery (CUMA and ETA renew their equipment fairly regularly). These autoguidance devices are more commonly found as original equipment than as retrofits (although retrofitting does allow for the addition of features such as guidance for a mounted implement, for example). CUMA and ETA employees can thus act as technical advisors, rather than referring customers to the dealer.

A limiting factor at the time of purchase could be the price and return on investment (ROI) at the time of purchase. The brand and model of the tractor may also be a factor (with on-board autosteering), in relation to monitoring, support, and commissioning of the machines. CUMA and ETA think in terms of working hours (unlike a farmer who might think in terms of purchase price), which favors this type of equipment. Using autosteering equipment would cost an additional €1 to €1.50 per hour of work, which seems acceptable to these delegation and mutualization structures, which often consider it a gain in comfort. However, tools such as autosteering do have an impact on the relationship with tasks, with the risk of falling asleep at the wheel or moments of inattention because there is “nothing left to do at the wheel” (or almost nothing).

Tractors equipped with this technology often work longer hours than those without it (whether with or without employees). Autosteering facilitates certain farming operations such as mowing, sowing, or working on narrow strips. In dry conditions that make it impossible to use a stubble cultivator after harvesting (due to dust clouds and large overlaps), autosteering allows the tractor to continue working on site. The human eye is not capable of maintaining a few dozen centimeters of overlap for several hours at a time if there have been shifts.

Otherwise, section control features seem to be fairly widely used, mainly in relation to non-treatment areas. Some go as far as implementing RTK geopositional tools for modulation or precision operations (apparently mainly under the John Deere and Trimble brands), but this phenomenon does not seem to be particularly widespread. The dynamics of the Centipede RTK open-source network also affect CUMA and ETA, except that dealers are not really supporting the movement, and are even hindering it by explaining that they will not help farmers to handle and configure Centipede beacons.

Some insurance companies are starting to make specific autoguidance contracts mandatory for new equipment in order to combat theft of these onboard tools. Given that autoguidance equipment is widely integrated into agricultural machinery as standard, farmers should be made more aware of this type of insurance contract.

Robotics: Robotics is still relatively absent from the CUMA/ETA landscape, although there are a few isolated examples. The CUMA in Aude is said to have purchased the first robot in the CUMA network—a Bacchus from Vitibot—mainly for mechanical weeding between rows in vineyards. The fact that these structures work on large, fragmented plots (because delegation or pooling is carried out among many farmers and therefore over large areas) may not be conducive to the use of robotic tools. However, the pooling of robots within CUMA and economic models based on rental and/or dedicated services using robots could be a solution to the high cost of this agricultural equipment.

Robotics may also raise questions for these structures regarding the redefinition of employee tasks, as employees may no longer need to operate machines if autonomous robotic units are invested in on farms.

DSS & Embedded Systems: There does not appear to be a significant trend towards the use of decision support tools (crop protection & disease risk, irrigation management, etc.) and embedded systems on agricultural machinery such as precision seeders, precision weeding with camera-equipped hoes, yield sensors, etc.

Some DSS are certainly becoming essential (e.g., Mileos for potatoes in France) to reduce the use of plant protection products, and practices such as irrigation management are raising concerns about rising energy costs (pumping water consumes energy) and the risk of water restrictions. However, these tools are not yet widely used in the day-to-day operations of these subcontracting structures.

The same applies to the modulation of cultivation operations, which is being introduced fairly gradually, without any major acceleration. Some CUMA members do use mapping services (usually for nitrogen) provided by their cooperative or on their own initiative. This nitrogen modulation is certainly the most widely used service, but it is far from being the only one. The purchase price of agricultural machinery can also be a good proxy for determining whether precision tools are included (e.g., on fertilizer spreaders).

Some agricultural contractors will still invest in equipment, particularly those with the most financial resources, in order to stand out from the competition and offer, for example, reductions in input use or compliance with environmental standards. This is also the case for large multi-service agricultural contractors who work on behalf of agricultural supply, agricultural machinery, or industrial companies. Investment in digital tools is greater in these cases, and partnerships are designed so that agricultural contractors do not always have to pay for this digital equipment.

Despite this, for equipped agricultural contractors, the data generated by these onboard sensors is not really analyzed. This is particularly striking for data from yield sensors (even though these sensors are very often fitted as standard on harvesters) – agricultural contractors do not want to bother with this. Once again, the use of digital tools is more of a marketing argument, or even an internal work convenience tool (see autosteering). In the context of the partnerships mentioned above (agricultural suppliers, agricultural machinery manufacturers, industrialists), it is sometimes these structures that will analyze and remotely control the data collected. Typically, a manufacturer will be interested in tracking data from combine harvesters to know when a plot has been harvested and when the crops will arrive at the factory.

Farmers may occasionally be interested in some of these digital tools—for example, to assess the fertilizing value of livestock manure (using on-board spectrometers). However, if demand is not guaranteed over time, implying that values are measured once “to see,” it remains difficult to recoup the investment for the subcontracting structure.

I have not received any information about machine adjustment DSS or digital tools for operator safety at work. All of this could be explored in a future quantitative survey. For further information, see some Aspexit blog posts:

- On standards and data exchange in digital (2021)

- On agricultural robotics (2022)

- On pest management

- On Irrigation control

- On nitrogen fertilization management

Some projects and/or players to know about

- In 2024, the INVIVO cooperative launched “Sowfields,” its new farm management assistance service.

- The DigiCUMA network highlights CUMA cooperatives that are pioneers in testing and using digital tools in real world conditions

- The online “Carto’Mat” map of mechanical weeding tools available in Brittany in CUMA and ETA cooperatives https://desherbage-meca.carte.bio/

- The CASDAR “Agroop” project, co-piloted by CUMA networks to disseminate and increase the use of digital tools that can be used in conjunction with agricultural equipment.

- The ETA trade show (organized by Profields)

Let’s take a step back

The problem of field data entry

The problem of field data entry—machine data and crop route data in this case—has been known for a long time. Manual data entry is prone to error, hence the widespread move to automate this information gathering process. As discussed in the section on digital tools for agricultural contractors and cooperative equipment associations (CUMA), companies offer devices that can be mounted on machines (magnetic, connected to the machine’s CAN bus, etc.) to collect this field data.

This strategy of devices is also a way of responding to the fact that many agricultural equipment manufacturers exploit their data for their own benefit. Some brands open up access, others close it, or even change their data management policies. While it is understandable that certain data may be confidential to the manufacturer (e.g., device data, i.e., data specific to the machine), other data such as user data (plowing trajectory, area worked, working speed, etc.) should be more easily accessible. I would like to take this opportunity to point out that the European Data Act, which will come into force on September 12, 2025, should bring about a better distribution of the value derived from the use of personal and non-personal data among stakeholders. More specifically, farmers should have easier access to the data sets produced on their farms and control how this data is shared with third parties.

Some manufacturers are quick to use telemetry to collect machine data and monitor the proper use of their agricultural equipment by farmers. This sometimes results in implements would not have been operated within the correct usage ranges. One interviewee told me that a CUMA president had received a call from his dealer asking him to come and change the oil in one of the CUMA’s tractors—the tractor’s operating data had been analyzed by the dealer in question, apparently without the CUMA president’s knowledge. Today, John Deere, for example, installs Telematics directly on its machines, and farmers are not always aware of this when they sign the machine delivery documents at their farms. Farmers remain the owners of the data, but the manufacturer retains the right to use it.

How should we respond to this trend? From a functional and usage-based economic perspective, it is understandable that a manufacturer would want access to the operating data of its machines—especially in the context of agricultural equipment leasing models. Operators and mechanics can then intervene directly on site with the right tools and save time. It is also a way of raising awareness among farmers who are members of a CUMA (cooperative for the use of agricultural equipment) or other cooperative structure about the use of their machines, and even of changing the internal regulations (perhaps even by machine) of these cooperative structures.

On the other hand, there is a risk that this data could be used by insurers and lead to the exclusion of certain insurance contracts (John Deere, for example, sells harvest forecasts based on yield sensors installed on its machines to banks and other organizations). Some insurers are already implementing specific contracts on machine autosteering to prevent an increase in thefts of these on-board tools.

For mutualization and subcontracting structures, the main objective of this automatic data capture using boxes is to focus on business aspects, namely the total number of hectares worked and the time spent on the work, in order to monitor costs and margins. A behavioral analysis of machine geodata (GPS data, machine type, vibration analysis) generally provides more or less detailed access to site indicators (start time, end time, mileage, time in motion and on break, etc.). For certain operations, such as soil cultivation, it is still difficult to know what the machine is actually doing. Vibration or revolution counters are less valuable.

These connected boxes tend towards zero data entry. Many of these box suppliers still seek to connect to parcel management software because agricultural contractors and cooperative equipment associations also need to manage schedules, monitor their machines (fuel levels, equipment maintenance, technical inspection notifications), and organize their invoicing (see the “Internal Tools” section), which the boxes cannot really handle on their own. I am not referring here “simply” telemetry, which is very useful for ensuring that machines are working properly remotely, but rather the data needed for the business management of delegation companies.

In order to produce billable work—especially if detailed traceability is required—farmers will inevitably have to edit certain information at some point: the stage of crop development and the crop being treated, the dose applied, price or VAT adjustments depending on the customer, the number of bales of pressed straw and their type (synthetic twine, hemp twine, wrapping, netting, etc.). This traceability may be even more important in the long term for completing mandatory government declarations or phytosanitary records (see the requirement to keep a digital phytosanitary record from early 2026). To what extent are these IoT tools capable of collecting this data in detail, either directly or by re-analyzing machine data? It should also be noted that this useful data may also be missing from the IsoXML files provided by tractor manufacturers.

At what point do these IoT tools compete with smartphone applications based on this management software? Management structures can effectively develop mobile applications (to report work orders from the field) by imposing a certain amount of mandatory data to ensure that agricultural projects, once reported in the management software, are billed correctly. And for collective management structures such as agricultural cooperatives, this is all the more interesting because it guarantees them consolidated data at the level of their members.

Are ETAs and CUMAs part of a general trend towards digitization in the agricultural world?

This was one of the main questions that motivated me to put together this report. Based on my discussions and reading, I would tend to answer: not really. Nevertheless, I would add a slight nuance in case certain weak signals might lead to a reconsideration of the answer.

As we have repeatedly pointed out, machinery represents a significant expense for agricultural operations. By equipping their agricultural machinery with certain digital tools, companies such as CUMA and ETA enable farmers to test or question the value of such digital tools before potentially investing in them. For some farms, perhaps small and medium-sized ones, these companies are a kind of foot in the door for the digital ecosystem because they sometimes introduce digital tools to these farms for the first time. The observatory of digital uses in agriculture gave the example of a farmer who switched from chemical weed control to mechanical weed control by introducing digital tools on his farm (Observatory of digital uses in agriculture, 2024). It is therefore not so much a test as a discovery of a potentially unknown set of tools. Other delegation structures purchase equipment for their agricultural machinery with the idea or hope of getting a better resale price when they leave.

The agricultural contractors and cooperative equipment associations that have purchased sophisticated or high-tech equipment do not seem to be particularly promoting it, at least for the moment. While these digital tools can help them stand out from the competition, contract farmers do not necessarily choose an agricultural contractor because it has a particular onboard sensor or modulation service. Nevertheless, given the increasing concentration of French farms and environmental imperatives (as discussed earlier in the blog), it is likely that farms that have expanded will have greater resources and will be very demanding when it comes to the work carried out on their land (compliance with specifications, etc.). So perhaps we are a little early.

From a very operational standpoint, CUMA and ETA often face peaks in workload or tight time frames. While certain digital tools clearly make their work easier (e.g., autosteering—the additional cost of section control and overlaps remains low), transferring data from on-board sensors (yield maps, nitrogen application maps, etc.) takes time and can slow down the work. The contractor sometimes arrives at the farm at full speed, with tight time constraints, and the farmer sometimes does not even have time to transfer his modulation file before the work is already completed. Better data interoperability (between clouds and between machines) could therefore lead to better agronomic consideration of field realities.

Unfortunately, agronomy is not yet the primary driver of transformation. Without going so far as to say that some agricultural contractors are not agronomists (I don’t want to get into trouble), I mentioned earlier that the landscape of delegation is multifaceted and involves a huge number of different players, some of whom are clearly not agronomists. Yield maps generated by onboard sensors can be used to calculate actual exports by soil type within the plot, enabling crop management plans to be reorganized by soil type (for example, by developing intra-plot fertilization plans using agronomic calculation engines). This advisory work takes time and is sometimes at odds with the profitability requirements and time constraints of delegated structures.

The reasoning of the CUMA may be slightly different in that the approach is more voluntary, with members seeking agronomy and technical expertise in these equipped machines. These farmers will therefore potentially be more curious and willing to spend more time on data transfer.

More generally, experience shows that selling technological tools in the field takes time. A sales force— trained and aware of these digital tools—is necessary. At the time of writing, I do not think that we can say that agricultural contractors and cooperative equipment associations are familiar with all the digital tools mentioned in this report—regardless of whether they view them favorably or not. What I mean here is that if we consider these structures as intermediaries for introducing or demonstrating the existence of digital tools to farmers, we need to spend time in the field presenting this ecosystem to them.

ETAs and CUMAs tend to work in a spatially localized manner. Traveling on the roads is expensive (with the price of GNR) and increases the risk of wear and tear and breakage of agricultural equipment (and with the high cost of machinery). It is therefore more likely that this agritech ecosystem will become known in the field through word of mouth, with one ETA/CUMA leading to another (Wang et al., 2022). If digital tools are deemed relevant, the absence of these types of agricultural businesses close to home may push farms to equip themselves internally.

Towards a reconfiguration of the agricultural world?

Are we in the process of changing and shifting towards a new model of “delegated agriculture,” with family farming giving way to outsourced labor?

Farmers are outsourcing more and more agricultural tasks (no less than 6 out of 10 farmers according to the latest agricultural census), especially when the farm is diversified and located near an agricultural contractor. This outsourcing due to a lack of capacity or resources sometimes leads to more advanced forms of outsourcing: strategic outsourcing to optimize resource allocation, refocus, or manage assets (complete delegation through “refocusing” or “abandonment”). Some farmers even use subcontracting as a means of diversification, before some of them switch to a new profession, that of contractor (Nguyen et al., 2022).

This trend is not limited to agricultural contracting companies, but extends to the entire delegation landscape (Figure 10). Traditional collective actors such as CUMA, agricultural study and technical centers (CETA), and agricultural cooperatives are also doing well and are reorganizing or forming alliances to stay afloat.

This subcontracting dynamic is far from easy to regulate. It calls into question the status of farm managers and what constitutes an active farmer. The status of tenant farming, considered restrictive by some farmers, may also have contributed to creating a context conducive to the development of subcontracting (sometimes on a full-time basis).

Full delegation contracts are more flexible and allow farmers to retain their assets and land while awaiting a possible sale or takeover in the medium or long term by a successor who has not yet been identified, or simply to supplement their income in the form of an annuity. Despite the risks borne by the farmer, who could see their subcontracting agreement reclassified as a farm lease or even lose their status as a farmer and thus their CAP subsidies, farmers prefer to delegate the management of their farm rather than lease it out, thereby distinguishing between productive capital and family assets (Nguyen et al., 2020, 2022). In general, this subject of contracts raises a lot of debate and it is interesting to see the analyses of lawyers compared.

The delegation is becoming more professional with the development of new subcontracting and delegated production relationships. New intermediaries are emerging (project management assistants or managers, known as “land managers” in some countries such as Belgium and England) who coordinate the subcontracting process (drafting contracts and monitoring their execution) and manage any conflicts between stakeholders. This was even the case on a fairly large scale. These “managers” were not usually hired. The relationship often took the form of a traditional service contract, annualized and tacitly renewed from one year to the next. For the sake of simplicity.

As delegation increases, those delegating are also becoming more demanding about the completion of work, wanting proof that the work has been done and done correctly, which sometimes leads to a need for increased traceability. These managers will also highlight promises that are not always focused on profitability for the customer, but also on compliance with specifications (e.g., low carbon footprint, organic farming methods, etc.). It is these intermediaries who will then organize the work between different agricultural contractors or downstream companies.

Could this management-driven approach to agriculture be indicative of a broader trend toward the tertiarization of agriculture, which is more pronounced than the industrialization of production units? Certain French departments run the risk of being abandoned if agricultural work is entirely outsourced, with a potential risk that production could be geared towards issues other than food, such as France’s energy sovereignty, because they are considered more profitable (production of energy crops). Outsourcing also carries the risk of increasing distance from the environment in which agricultural activity takes place.

An additional fear of this phenomenon of tertiarization, as experienced in other economic sectors, is the impoverishment of certain professions, with operators dedicated to driving machines without a meaningful understanding of the ecosystems being cultivated. Several authors seem to highlight the development of precarious employment in subcontracting companies: employer groups, agricultural contractors, and the development of posted workers. Nevertheless, this is an argument for maintaining agricultural jobs in certain rural areas.

Some large agricultural contractors are beginning to acquire very large tracts of land. While statistics are not always available, the increasing number of employees in these structures could serve as a proxy. Some of these companies also take advantage of privileged relationships with future retirees or farmers nearing retirement to acquire land once the owner or tenant farmer of the land has legally ceased their activity. Taking this idea a step further, these large, multi-service structures (or the managers mentioned above) actually control the organization of production across an entire region.