Carbon is the only word on everyone’s lips. Finger-pointed as the evil of the moment – due to climate change – we almost forget that we are made of it. We should stop emitting it, transforming it or storing it – we don’t want it to show its face. And the subject is a hot one in agriculture. It is one of the sectors that emits the most greenhouse gases, but also the one that has the greatest potential for storing carbon in its simplest form, the soil. It is a sad paradox that the atmosphere contains too much carbon while the soil lacks it.

Carbon measurement tools, models and monitoring methods are being developed. Labels and certification frameworks are emerging. A carbon market is being established. We will focus here on agriculture, of course, but we will allow ourselves a few digressions on the forestry sector. As a source of motivation or inspiration for some and concern for others, the subject of carbon is not unanimously supported. The fact remains that the subject is fascinating. Between climate advocates, agriculture advocates, and opportunists, carbon has a way of making heads spin.

As usual, for readers of the blog, this article is based on telephone interviews with players in the sector (whose names you will find at the end of the article), whom I would like to thank for the time they gave me. Several articles, reports and seminars have enabled me to complete the feedback from the interviews.

PS: I always give a digital prism to my articles since I work in the field of digital tools applied to agriculture. You will also find it here, but to a lesser extent than in other articles I have written in the past.

PS2 : Be aware that the article relates more to France and Europe than in the rest of the world.

Soutenez Agriculture et numérique – Blog Aspexit sur TipeeeLegal references – Laws and regulations

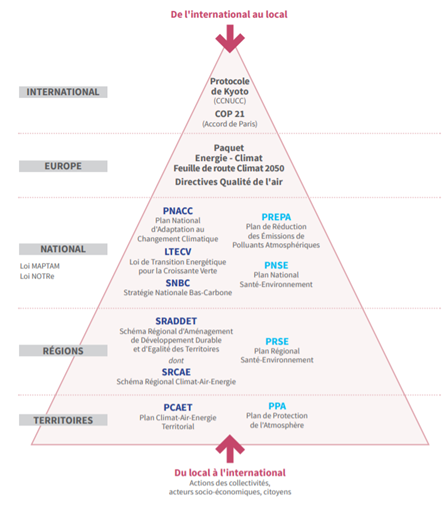

There is no longer any doubt that climate change is at work. The terrible frost episodes observed in France at the beginning of April and the destruction of almost the entire village of Lytton in British Columbia by fire at the end of June will certainly have convinced the last sceptics. The IPCC (Intergovernmental Panel on Climate Change) and other international bodies keep hammering it home with ever more alarming reports. The number of objectives, protocols, agreements and strategies put in place over the last few years to guide international and national trajectories towards a reduction in greenhouse gas emissions has been countless. Who really knows where we stand? There have been so many of them that it is difficult to find one’s way around. A few points of reference can’t hurt. This part is not very sexy, but it will have the merit of restating climate policies and introducing certain acronyms that we will need later on. We’ll discuss the mechanisms, emission allowances, and carbon markets associated with all this later in this article. I promise you, we will be talking about agriculture very soon.

At the international level, it was the United Nations Framework Convention on Climate Change (UNFCCC) that set the ball rolling in 1992 (it was adopted in 1994). Signed at the Rio Earth Summit by nearly 190 countries, the convention’s main objective is to stabilise greenhouse gas concentrations “at a level that would prevent dangerous anthropogenic (human-induced) interference with the climate system”. Although the proposed ambition was very commendable, it must be admitted that the framework was still rather vague. Nevertheless, the convention had the great merit of highlighting the responsibility of the industrialised countries for climate change, and of pushing these countries to take the lead by doing their utmost to reduce emissions on their territory. It was not until a few years later, in 1997, that the Kyoto Protocol finally clarified the legally binding emission limitation and reduction obligations of industrialised countries. Over the first Kyoto Protocol period (2008-2012), the industrialised countries that signed the protocol – the so-called “Annex I” countries – committed themselves to reducing their greenhouse gas emissions by an average of 5%. The other signatories, but non-industrialised countries, known as ‘non-Annex I’ countries, have not committed themselves to any emission reductions so that they can continue to develop. The attentive reader will have noted the time taken between the signing of the Kyoto Protocol and its first period of application. A second period of application of the protocol (2013-2020), the Kyoto Protocol II, will set as a common objective for the signatory countries a 20% reduction in their emissions by 2020 compared to the base year 1990. This extension of the Kyoto I Protocol will be narrowly concluded at the Doha climate summit in 2012, as previous COPs and climate summits, notably the Copenhagen summit in 2009, had failed to reach a consensus. It should be noted that some of the countries that signed the first Kyoto Protocol had in the meantime withdrawn from the second… The Kyoto Protocol ended in 2020! It was replaced by the Paris Agreement, signed in 2015 at the COP21, which came into force on 1 January 2021. Considered historic, the Paris Agreement is the result of a common understanding among its signatories on the importance of limiting global warming to well below 2 degrees Celsius, preferably 1.5, above pre-industrial levels. The Paris Agreement remains an agreement, however, without any constraints. The increase in greenhouse gas emissions between 2015 and the start of the Covid-19 pandemic should not completely reassure us… Let’s conclude with a good point for the agricultural sector: carbon storage in the soil was recognised as a means of combating climate deregulation during COP23 under the United Nations Framework Convention on Climate Change.

At the European level, in 2020 we saw the arrival of the European Green Deal, whose initiatives aim to make Europe the first carbon-neutral continent by 2050, no less. Initial greenhouse gas emission reduction targets have been set within the European Union for 2030, with emission levels at least 55% lower than in the 1990s. This Green Deal follows on from the Energy and Climate Package (also known as the ‘energy-climate package’), which included a target to reduce greenhouse gas emissions by 20% by 2020 compared to 1990 levels. The Green Deal has therefore increased these ambitions for 2030. In agriculture, the European Green Deal has been translated into the “Farm to Fork” strategy, with a strong commitment to reducing the use of fertilisers, pesticides and antimicrobials. On the carbon side, the Farm to Fork strategy was an opportunity to consider carbon market systems to finance carbon offsetting in the agricultural sector. We will come back to this later in the article! The Green Deal and the Farm to Fork strategy should also serve as a framework for the guidelines of the new CAP, which should come into being during 2021-2022. Green credit schemes (eco-schemes, eco-conditionality…) are expected. Each member state will have to define its National Strategic Plan for the CAP (NSP CAP). For France’s NSP CAP, two levels of credits (standard and higher) should be accessible through three access routes: practices [improvement of existing practices such as plant cover or crop diversity], environmental certification [use of existing certification frameworks such as HVE or organic], and agro-ecological infrastructures also known as AEI [implementation of elements favourable to biodiversity]. The level of the amount of these green credits is not yet fully decided.

At the national level, Cocorico, France has put in place its law on the energy transition on green growth (LTECV) in 2015. This law aims to reduce greenhouse gas emissions by 40% compared to 1990 and to reduce fossil fuels by 30% compared to 2012. The LTECV gave a general orientation which was then accompanied more recently by a roadmap to fight climate change, the National Low Carbon Strategy (SNBC). In this framework, greenhouse gas emissions are to be halved, including in the agricultural sector – and carbon storage is also widely considered. The national low-carbon strategy complements and is linked to the national plan for adaptation to climate change (PNACC) programmed following the Grenelle Environment Forum. And it is also within the framework of the SNBC that the “Label Bas Carbone” was launched (we will come back to this later). In May 2021, France ratified its “Climate and Resilience” law, following the proposals of the Citizens’ Climate Convention (3C). These proposals included several articles on agriculture and food. The Climate and Resilience Law is currently being criticized quite a bit, especially by the citizens of the Citizens’ Climate Convention, who gave it a nice score of 3.3/10. Not exactly reassuring… On the agricultural side too, former agriculture minister Stéphane le Foll launched the international 4/1000 initiative in France in 2015, or to put it another way, the annual increase of the carbon stock in the world’s soils by 0.4%. Intrinsically linked to the SNBC, and by the same token to agriculture, one could also add the National Biodiversity Strategy (SNB) – biodiversity whose decline has been widely pointed out by the IPBES (Intergovernmental Platform on Biodiversity and Ecosystem Services), and the “Net Zero Artificialisation” (ZAN) strategy for soils by 2030. Following the Covid-19 pandemic, the French government deployed its recovery plan (called France Relance), which includes several measures in favour of the energy and climate transition. These include the Carbon Diagnostic Vouchers, which we will discuss later in the article.

To go a little further into this mishmash, and if you haven’t had enough, I suggest you take a look at the following graph, taken from an ADEME report. It shows the link between several of the strategies and objectives presented above.

Figure 1. International and national policy to combat climate change.

Carbon stocks and flows

The subject of carbon in agriculture is rather paradoxical. We are constantly told that there is too much carbon in the atmosphere, yet we are trying to increase the organic carbon content of soils. And for good reason, decades of chemical agriculture and intensive modern techniques will have led to a loss of 50-70% of carbon stocks in our largest storage compartment, the soil. The IPCC reports estimate that there are around 1,500 Gigatonnes of carbon in the soil, which is about three times more than what is found in the atmosphere, but with a large margin of uncertainty. Add to this the fact that carbon stocks are often measured down to a depth of 1 metre, whereas even more could be found by digging a little deeper. With climate change on the rise and carbon levels in the atmosphere rising dramatically, the subject of carbon storage has become particularly topical, in the sense that it could help solve the climate equation. However, it should not be seen as a quick fix and it should be remembered that storage will never replace emission reductions at all possible scales, including for agriculture.

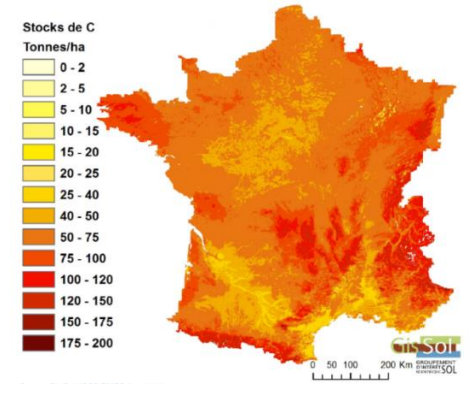

Figure 2. Map of French soil organic carbon stocks (in tonnes of carbon per hectare) in the first 30 cm of soil (GIS Sol data). Not all countries have carried out this carbon stock survey

The main carbon storage process in the soil is photosynthesis. It is this absolutely incredible process that enables the transformation of atmospheric carbon into organic carbon in the plant; carbon that will then be stored in the soil when the plant biomass, loaded with carbon, decomposes (cover residues, roots, litter…). This carbon, contained in the organic matter of the soil, will be found in the soil in several forms, more or less easily degradable or mineralizable. In particular, there will be labile forms of organic matter, which can be mineralised fairly quickly by the soil micro-organisms to ensure soil fertility and the circulation of carbon throughout the soil food web, and intermediate or stable forms which will remain in the soil over long periods of time.

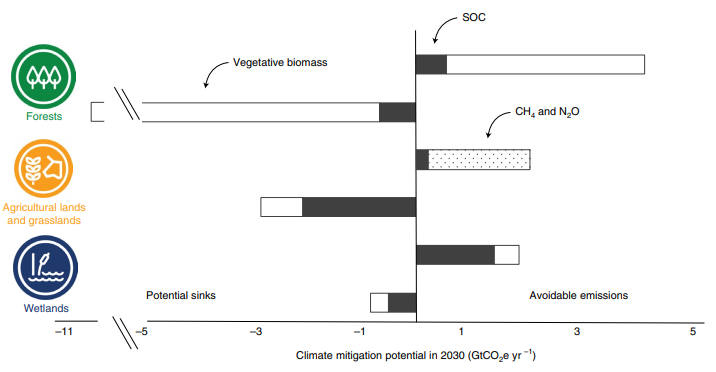

Figure 3. Maximum climate change mitigation potential of soils in 2030 in the pathways of the forest, agriculture and grassland, and wetland biomes, with safeguards. To the left of the vertical bar are the mitigation potentials through storage. On the right are the mitigation potentials through emission reductions. The dark parts of the bars represent soil organic carbon. The white parts represent vegetative biomass and the dotted part represents CH4 and N2O avoided through better nutrient and animal management. Source: Bossio et al (2020).

It is important to understand that carbon in the soil follows a dynamic, it is a continuous inflow and outflow. Carbon is stored in the soil by the addition of organic matter (endogenous or exogenous to the farm) and is removed by mineralisation of the organic matter. The challenge is to ensure that carbon stocks (especially intermediate and stable forms) increase as much as possible and remain in the soil as long as possible. We are talking here about the effect of reversibility or non-permanence of carbon in the sense that everything that has been stored can be destocked if so-called “destocking” practices are implemented on the farms. Hence the primary motivation to preserve as much carbon as possible where it is abundant, and in particular to avoid deforestation, the turning over of forests, or the drainage of organic soils and wetlands.

It should be borne in mind that carbon levels in the soil will always eventually reach a state of equilibrium (except in certain special cases), i.e. the levels of carbon entering and leaving will be the same. As storage progresses, adding more carbon to the soil will become more and more complicated, but the challenge will be to store as much as possible. However, it is not enough for a soil to be rich in carbon to be alive and highly functional. It is the autonomy of fertility and the capacity of the carbon to be well integrated into the soil network that should be sought. As someone else would say, if you just want to add carbon to the soil, you can bury used tyres in it…

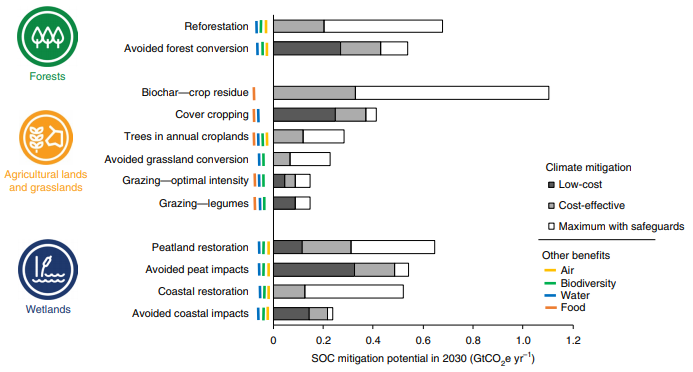

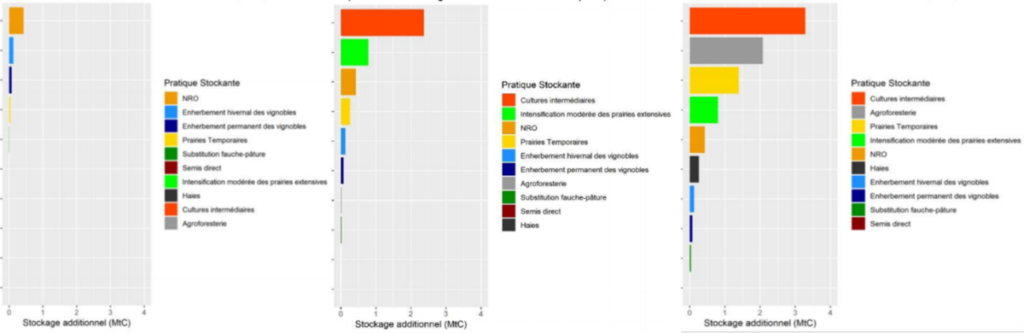

And these stocking or destocking practices are beginning to be widely known and documented. In agriculture, although some of them are still the subject of heated debate – particularly the effect of no-till – there is a consensus on many of them: introduction of cover crops, agroforestry, management of temporary grasslands, etc. (Figures 4 and 5). We can then differentiate between practices that are more in the nature of optimising existing practices and those that are more transformative, where the farming system is really undergoing a profound transformation (introduction of cover crops, for example). These practices have a more or less marked interest in soil carbon storage, and are above all more or less costly to implement (Figures 4 and 5).

Figure 4. Additional SOC storage potential for 12 natural climate mitigation pathways. The dark grey part of the bars indicate low-cost mitigation levels (<10 US dollars per MgCO2e per year). The light grey parts of the bars represent cost-effective mitigation levels under the assumption of a global ambition to keep warming below 2°C (<100 USD per MgCO2e per year). The white parts represent the maximum additional storage on top of these two previous bars.

Figure 5. Contribution of practices to the additional storage obtained for a carbon price. On the left for 0 €/ tCO2e, in the middle for 55€/tCO2e, on the right the maximum additional storage. Source: INRAE (2019).

What is the soil storage potential? There are actually several ways of looking at it. It could be seen as a biophysical potential (what could be found under a forest or a permanent grassland) or a technical potential (what is technically possible), which are the references that are most used. But we could also define this potential from an economic point of view (the practices have a cost to be implemented) or an achievable point of view (ensuring that the practices are adopted, and setting up an environment that is favourable to the development of low-carbon projects: training, support, networks of actors, tools available, financial incentives, etc.). We will discuss this further below.

The storage of organic carbon is an issue in the fight against climate change, but it should not be considered only from this perspective, quite the contrary. It is the number one factor in all the functions that the soil can perform in the first few horizons: maintaining fertility, reducing soil erosion, structuring and carrying the soil, etc. The carbon issue is therefore a co-benefit that must be taken advantage of, but for which the soil cannot be summed up.

Different types of emissions and Scope 1 – Scope 2 – Scope 3

So far, we have talked a lot about carbon storage in the soil. To come back quickly to the part on emissions in agriculture, they are mostly known and well identified. In the French sector, agriculture is in third place with almost 20% of French emissions. The main culprits are carbon dioxide (CO2), methane (CH4) and nitrous oxide (N2O). And it is CO2 that is emitted in the greatest quantity. The problem, however, is that methane and nitrous oxide have far greater warming effects than carbon dioxide. This is a factor of 25 for methane and a factor of 300 for nitrous oxide. One unit of CH4 can therefore be converted into 25 units of CO2 equivalent, and one unit of N2O can be converted into 300 units of CO2 equivalent, so that all greenhouse gas emissions can be compared on the same basis (we will therefore speak of tonnes of carbon equivalent or tCO2eq for short). Even if they are emitted in smaller quantities, it is difficult to ignore methane and nitrous oxide… The main emissions are due to the enteric fermentation of ruminants, the manufacture and use of nitrogenous mineral fertilisers, the use of diesel to power agricultural machinery and changes in land use. These emissions are well documented in the literature.

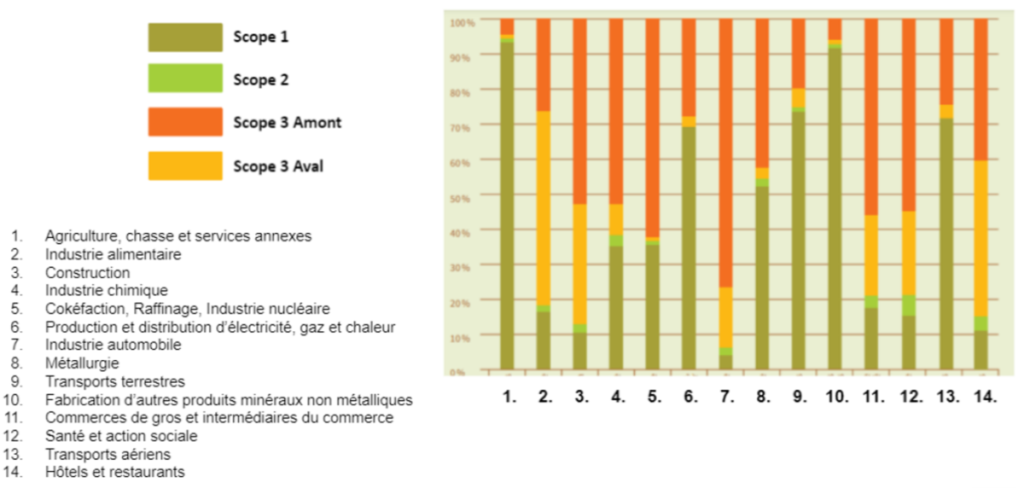

One way to characterise the emissions of a farm or business is to think in terms of “scope”. There are three different scopes – Scope 1, Scope 2, Scope 3 – which Ademe (French Agency for the Environment and Energy Management) defines as follows:

- Scope 1: Direct emissions from sources owned or controlled by the organisation: combustion from fixed and mobile sources, non-combustion industrial processes, ruminant emissions, biogas from landfills, refrigerant leaks, nitrogen fertilisation, biomass, etc.

- Scope 2: Indirect emissions associated with the production of electricity, heat or steam imported for the organisation’s activities.

- Scope 3: Other emissions indirectly produced by the organisation’s activities that are not accounted for under 2 but are linked to the entire value chain, such as the purchase of raw materials, services or other products, employee travel, upstream and downstream transport of goods, management of waste generated by the organisation’s activities, etc.

When we talk about emissions, we are often only interested in Scope 1 and 2, either because they are simpler to calculate or because they avoid asking too many questions about what happens upstream or downstream of the operation or company. However, Scope 3 emissions are often far from negligible! And they vary greatly depending on the sector under study (Figure 6). For agricultural production (number 1 in the figure), it is not surprising that Scope 1 remains the priority, since the majority of emissions take place on the farm. But for the food industry (number 2 in the figure), this is no longer the case…

Figure 6. The different Scope levels.

Not taking into account Scope 3 can lead to completely biased results. Many companies or territories point to reductions in greenhouse gas emissions in recent years, but this is only because they are not considering their Scope 3, which would then completely reverse the trend. Forgetting about scope 3 often gives the artificial impression that we are on the right trajectory for reducing greenhouse gas emissions. However, we can see that a large number of the things we use on our territory are not produced there, which means that there are emissions that need to be accounted for (we are talking about imported emissions, such as the import of feed for livestock, which leads to deforestation in the countries producing the feed; this deforestation is therefore indirectly imported). One could also define the concept of avoided emissions, which is best understood as emissions that could be prevented by implementing a project (e.g. avoiding de-stocking practices or preventing a forest from being deforested). Combating climate change therefore requires attention to reductions in all these direct and indirect emissions.

Monitoring carbon emissions and storage

Measuring carbon in agriculture

To improve a system, you have to measure it; for me, this remains a fairly relevant leitmotif. In the case of carbon, what we would like to measure in order to do things properly are carbon emissions on the one hand and carbon storage in the soil on the other. Emissions in agriculture are not so much a problem. Let’s be clear, it’s not that there are no emissions, on the contrary – carbon dioxide, methane, nitrous oxide, among others – but it’s that, overall, we know them. There is an enormous amount of literature on the subject, databases of emission factors (how much this or that product or practice emits). And these databases are still being improved. In other words, we know more or less what we are dealing with. The big part of the current problem is monitoring carbon stocks in the soil. We know how to measure carbon in a soil sample at a given time. Quite classically, we analyse the organic matter content of the sample in the laboratory. The carbon is measured and a result is generally given in terms of organic matter (the proportion of carbon in the organic matter is fairly stable, so we get by). You can obviously go further by analysing different forms of organic carbon and different forms of organic matter, but that’s not the point (or at least not for the moment). But assessing carbon stocks on a larger territory (a plot, a farm, etc.), and especially monitoring the evolution of these carbon stocks over time, is a different matter. The physical measurement of this carbon has a cost, or rather several.

Firstly, there is a cost to sampling – in terms of time and manpower. A sufficient number of samples must be taken from a plot to be exhaustive and representative of the variability of organic content at a given time, which must then be sent (and paid for) to the laboratory for analysis. And for some, this spatial variability, sometimes even within a plot, is so great that the quantity of samples to be taken would be almost impossible to achieve (several hundred samples per hectare). However, not everyone thinks so, with some stakeholders questioning the quality of current sampling. For the latter, it is necessary to carry out soil analyses at constant bulk mass or constant bulk density, but especially not at constant depth, so as not to bias the results – and soil sampling would then be more than sufficient.

In order to monitor organic matter levels over time, regular sampling campaigns would be necessary. This could be done on an annual basis, along with other conventional soil tests, or at each key stage of a project to introduce carbon-storing practices – particularly at the beginning and end of the project. One of the main problems with this temporal monitoring is that changes in soil organic matter content would be too small to be detected properly. In other words, over short timescales (of the order of only a few years) the changes in organic content in soils would be smaller than the uncertainty of the laboratory measurement of carbon. In the introduction to this section, I made it clear that there was no technical issue with laboratory carbon measurement – we know how to measure content – but I did not say that the measurement obtained was extremely accurate. In fact, you would have to wait at least 6-7 years to detect significant variations in OM in the soil and make sure that you are not in the uncertainty range for laboratory measurements.

How, then, to avoid these two main problems, namely the quantity of samples required to correctly represent a plot or a farm, and the low temporal variability of carbon in soils, which would prevent temporal monitoring. A first, fairly classic response in science is modelling. Starting from a known initial stock of carbon in the soil, we model, from experimental data, how the farmer’s practices on site would influence the storage or removal of carbon in the soil. The model thus gives an average trajectory of carbon, and this trajectory can be given at the plot, crop system or farm level depending on how the modelling is carried out. We are therefore more in a logic of means (we look at what is done, we look at the means used) and not really in a logic of results (we observe what we obtain at the end), even if nothing prevents us from checking again at the end that the modelling has not been nonsense. One can very well imagine rather hybrid approaches in which data collection is carried out on an ongoing basis, allowing the modelling to be regularly adjusted to what is observed in the field (this is known as data assimilation). Let us also add that modelling is not necessarily static (the modelling parameters are fixed at the outset) but can also be dynamic (one or more modelling parameters are measured over time). Nevertheless, modelling cannot do without an initial carbon stock measurement so that the reference state is at least known with the best possible accuracy.

As the measurement of carbon stocks in absolute terms is already somewhat uncertain, there is a tendency to work on variations in stocks – a relative evolution of carbon, shall we say – rather than on changes in stocks in absolute terms. This is what one of the latest INRAE reports on the subject recommends (Yogo et al. 2021). In the framework of the AMG model tested (we will come back to all these models shortly), we can see in particular that monitoring stock variations rather than absolute stocks makes it possible to reduce modelling errors quite considerably. It is therefore preferable to say that in 5 years, the soil has stored 3 tonnes of carbon, rather than trying to estimate the output stock with precision. It is therefore a variation, a delta, or a differential that is perhaps more relevant to measure.

To compensate for the exhaustiveness of field sampling for monitoring carbon in soils, several players have positioned themselves on data acquisition systems. The main one is the satellite, whose images are taken regularly and cover relatively large areas. I will not dwell here on explaining all the characteristics of an image. The curious or neophytes can go and dig around the spatial, temporal, and spectral resolutions of the main satellite constellations used in agriculture. Keep in mind that in the context of carbon, the satellite image could be used for two things. Either to directly measure a carbon stock in soils by combining the different spectral information of the image, or to follow over time a parameter of interest integrated in a soil carbon estimation model (biomass in particular). At present, the satellite seems to be of more interest for its temporal dynamics and its monitoring of input parameters for agronomic models than for an absolute carbon measurement in due form, for several reasons. The image already gives a superficial view of the soil, whereas organic carbon is generally studied at soil horizons of 0-30 cm or even much deeper. The satellite signal does not penetrate many of the soil layers. The switch from optical to radar signals is not likely to help matters much. And the satellite is also faced with relatively small changes in soil carbon content over time. If variations are difficult to detect in the laboratory, they are even less likely to be detected by satellite. Some work in France is nevertheless interested in satellite tools for measuring surface organic carbon levels (Vaudour et al., 2021). In the near future, however, one might wonder whether this work will still be relevant for agricultural areas if all farmers have their soils permanently covered – the satellite will then no longer be able to observe bare soil colour to measure the level of organic matter on the surface. Besides, once you put carbon into the soil, the soil becomes darker, and it has a lower albedo. Once you store carbon in the soil, you would have to cover the soil to prevent the benefits of storage being lost through these albedo effects. Satellite work is based on the analysis of spectral information in the image, known as spectrometry. Similar approaches to spectrometry, but very close to the ground, are also being deployed. On-board spectrometers – for example the Verris technology used in France by players such as PreciField – or portable spectrometers are used to measure organic matter levels in soils. One of the main limitations or points of attention of these systems is the calibration of the sensors and the dependence of the spectral signal on soil conditions (water content, structure, etc.).

If large-scale sampling capacity is not technically or economically feasible, is it then better to monitor relatively few samples but always at the same location and over a long period of time, or to model the evolution of carbon content in soils using dynamic soil or vegetation parameters that can be monitored by spectrometry? Is soil monitoring on a very precise GPS point in time really possible insofar as the passage of machinery (even without tillage) and climatic agents can move some soil? We could also add that soil sampling is very concrete, and that it is something that speaks to farmers. It allows us to lay a certain number of foundations. For the deployment of a carbon reduction and storage dynamic in agriculture, there is a need for simple field indicators to be put in place on the farms. The organic matter content has the great advantage of making people think and move forward. As far as modelling is concerned, one thing is certain: on-site data are fundamental, particularly for initialising models. And modelling will be all the more accurate if it is possible to intelligently combine field measurements (initial carbon stock), farmers’ data (practices, interventions, etc.) and satellite data (dynamic monitoring of parameters of interest).

Market Models, Tools and Methods

Some terminology

Let us begin by clarifying a few terms. We will try to stick to them as much as possible in the rest of the document, but this will at least be an opportunity to provide a framework so as not to get too lost.

- The term “data” will already include anything that is used in any way to quantify or describe carbon levels or contents, and several of these have already been mentioned in the previous section. Example: samples, laboratory measurements, and to which we can add farmers’ data, soil databases…

- Then come the models which, as described, are based on a set of experimental data, and whose objective is to estimate the content or evolution of carbon content over time. It is important to check the conditions of applicability of the models (according to soil types for example). Example: AMG, SAFY-CO2, RothC, STICS, CHN…

- These models can be integrated into tools, which are in fact nothing more or less than a sort of slightly more human interface for the model(s) integrated into them. We can therefore, for example, parameterise a tool, have it tested by a user, and so on. Keep in mind that a tool does not necessarily use a model. It can simply use data from measurement systems, or carbon emission factors. Some tools and/or indirect models focus on carbon emissions while others will focus on soil carbon storage. Some focus only on carbon, while others will consider a wider range of greenhouse gases, including methane and nitrous oxide. Some tools may be certified (Ecocert, ISO, 2BSvs…), others not. Some tools may have several data entry modes (a very simple but coarse data entry interface, and an advanced data entry interface for more detailed results). Example: Simeos-AMG, MyEasyCarbon, Carbon Track, Cool Farm Tool, CAP’2ER, Systerre…

- The methods provide a framework for projects that aim to reduce emissions or implement carbon storage practices. Some methods can be certified, others not. In the context of carbon, a clear distinction can be made between environmental certification (which will tend to target a farm – it will be said to be in the process of progress) and environmental labelling (which will tend to target a product). Methods can be considered as standards if everyone considers them to be a reference. Methods may or may not recommend measurement tools. Methods may or may not comply with national or international recommendations or reports (GHG Protocol, IPCC). Example: Label Bas Carbone, Carbon Agri, Carbocage, ABC’Terre, Gold Standard, Verra VCS, Regen Network…

To compare the different tools, one way is to use the hierarchy proposed by the IPCC under the name of “Tier”. Tier 1 corresponds to tools that use emission factors from very generic models, which are not specific to a country or region. For example, such an agricultural practice stores or emits so many tonnes of CO2. Tier 2 goes a step further, with emissions factors that are often a little more specific to the country, region or condition in which the practices are implemented. Tier 3 tools are the most advanced and make use of dynamic carbon models (soil and/or vegetation parameters are followed over time to refine the models). The idea in general is not to say that this or that tool is better than the others – it can be used for that too – but rather not to compare cabbages and carrots. If we can, for example, avoid emission factors, we can find interest in going for Tier 3 tools. Within the framework of a territorial dynamic, it may be relevant to use what we know how to do with dynamic satellite monitoring.

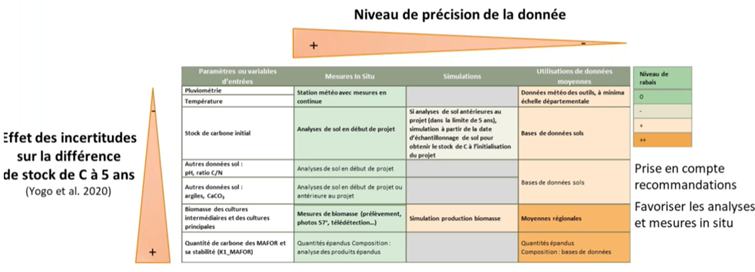

To compensate for the quality or uncertainty of the available data that may or may not be used to feed models and/or tools, several methods have set up a discount system. These discounts are often recommendations, as in the case of the Label Bas Carbone arable farming method, which should be officially validated in mid-2021 (Figure 7). These discounts are in addition to mandatory discounts for the risks of non-permanence of carbon in soils (we will come back to this later). Each method decides, guides or proposes how to consider the discounts.

Figure 7. Example of the calculation of the discount linked to the uncertainty of the input data of the soil carbon storage models for the Label Bas Carbone arable crop method. Source: AgroTIC Chair and Elsa-Pact Chair seminar.

Without being exhaustive, let’s go into the details of some French and international methods and tools. To complete these details, you will find comparison tables and tool and method sheets in a recent INRAE report (Yogo, 2021).

The Label Bas Carbone method: LBC

The Label Bas Carbone (LBC) method is a government-sponsored strategy under the auspices of the French Ministry of Ecological Transition and Solidarity (MTES), in support of the National Low Carbon Strategy (SNBC). It is a government initiative to encourage French farmers to reduce their emissions and implement carbon storage practices, and to encourage French and international companies to take an interest in projects carried out on French territory. The aim is to provide guarantees on the ground and to seek remuneration for these emission reductions. It is an incentive to implement low-carbon practices.

Depending on the sector and context, the LBC method has either been deployed, is being deployed or is being developed. For example, there are variations on livestock farming (the method is called Carbon Agri), field crops, vines, orchards, hedgerows and methanisation plants. It is not the ministry or the agro-industries that impose new methods but the players in the sectors that propose these methods. For each of these sectors, the consortium, agricultural professions, federations or technical institutes mobilised are different.

The LBC method is a voluntary carbon certification framework for private projects. Each structure or group of farmers (the LBC method does not really target individual farmers) wishing to have their emission reduction or storage project certified can set up their project and apply to the Ministry of Ecological Transition. The ministry is not really looking to target individual projects but rather to aggregate a critical mass of farmers to collectively seek funding. Only projects on French territory can be labelled by the LBC. Following a project labelled by the LBC method, it is the emission reductions that will be certified and not the farm itself. A farm that embarks on an LBC certified project will not be certified as a low carbon farm. What will be certified is the fact that the farmer’s practices have reduced emissions and/or stored carbon in the soil. Once recognised and certified, the emission reductions can be marketed, the so-called “carbon credits”, to which we will return later. The carbon reduction units are the property of the project owner (farmer or forester)

The LBC method is an obligation of means, there is no obligation of results. An initial diagnosis is carried out on the farms by collecting field measurements and data from farmers. These data are then used to define a reference scenario. This scenario will finally be projected into the future after modelling with the farm’s current practices, and will be compared to one or more scenarios that are also theoretical but use more virtuous practices on the farm. It is the difference between these two scenarios, both projected, that will allow the assessment of the emission reductions and/or carbon stocks on the farm. Be clear that the scenario with virtuous practices is not compared to the reference state at the time of data acquisition, but to the reference state projected in time, considering that the practices on the farm do not change. For the soil carbon storage part, the absence of an obligation to achieve results does not require a return to the field to establish a new state achieved. The modelling is sufficient in itself. The LBC method considers that if the agronomic levers are applied, the project is necessarily heading in the right direction.

On the emissions side, the reductions are evaluated at the end of the project by studying the farm’s invoices (consumption of nitrogenous mineral fertiliser, fuel, etc.).

The LBC method is suitable for all types of farming profiles, whether it is someone who has not implemented any virtuous practices, or on the contrary, someone who is already very committed to reduction or storage practices and who would like to have what has already been put in place recognised. The difference will depend on the reference scenario chosen. Let’s take the example of carbon storage. In the first case, where it can be assumed that the margin of progress is significant (we will speak rather of additional carbon storage), the farmer can compare himself with or without practices. This farmer, perhaps going from 50 to 52 tonnes of carbon in his soil, will have stored 2 tonnes. In the second case, where the margin of progress is already more limited (we will speak rather of maintaining stocks), the farmer will be better off choosing a generic reference – such as an average on farms with similar soil and climate conditions to his own. A farmer who already has a stock and who will maintain it over time will therefore be able to have it recognised. The objective is to have him maintain his practices to avoid destocking carbon. This farmer, for example, who already has a soil stock of 52 tonnes of carbon, will avoid falling back to 50 tonnes of carbon if he stops his storage practices; he will then have avoided destocking 2 tonnes.

The LBC method looks at the farm and/or cropping system scale, but it does not consider each crop independently.

At this stage, the LBC method is not linked to the CAP.

The CAP’2ER tool

The CAP’2ER tool is the Carbon Agri method tool, which in fact corresponds to the LBC method for livestock. Set up by the CNIEL and IDELE, the Carbon Agri method has been submitted to the Ministry and certified in September 2019. The CAP’2ER tool did not come out of nowhere. For nearly 10 years, IDELE and its partners have been working on the issue of agricultural impacts on the greenhouse effect, air quality and the preservation of energy resources through the Ges’tim project, which will also be updated soon.

The first carbon project deployed in 2019 – Carbon Diary – made it possible to carry out a carbon diagnosis on 4,000 farms with the CAP’2ER tool. Today, by mid-2021, there are 15,000 farms involved for 22,000 diagnoses (some farms have already carried out two diagnoses)

In the same vein as the LBC, the Carbon Agri method is a voluntary approach, the aim of which is to involve as many producers as possible. The CAP’2ER tool is a Tier 1 tool, based mainly on emission factors and empirical data from the literature. Although it also looks at carbon storage in soils through grassland use, its main contributions are on greenhouse gas emission reductions, carbon dioxide, methane and nitrous oxide.

We will discuss carbon credits later, but in the context of the emission reductions generated by the Carbon Agri method and to manage the carbon reduction mechanisms, the “Jeunes Agriculteurs” (Young Farmers) have created the France Carbon Agri association, of which IDELE is the technical operator. Unlike livestock farming, where the project agent – France Carbon Agri – is very well identified, the field crop sector will see many different agents (Coops, CETA, GIEE, CER, consultancies, etc.) to develop collective projects for farmers. The operation will be the same but this ecosystem will be much more fragmented and decentralised than it is in the livestock sector.

A European version of CAP’2ER is under development.

The SAFY-CO2 model

Developed by the CESBIO and the CNRS, the SAFY-CO2 model (or SAFYE-CO2 when a water component is integrated into the model) is an agro-meteorological model whose objective is to estimate carbon storage by the plant, by making a direct link between this storage and the biomass observed by satellite. The use of Sentinel 2 satellite data makes it possible to show the carbon balance of the year (CO2 fluxes and carbon exports at harvest) at a plot scale. Note also that the model does not stop at biomass but is also interested in yield estimation. As you may have understood, the SAFY-CO2 model is a Tier 3 approach.

For the moment, SAFY-CO2 is only parameterised for four crops (wheat, sunflower, maize, rape) with a rather generic parameterisation, which can nevertheless evolve according to the type of cover present. For winter crops, two parameterisations are available, one for short cover crops (mandatory cover crops in relation to the nitrate directive) and another for long cover crops, those destroyed at the end of March or beginning of April. For summer crops, the task is a little more complicated insofar as the distinction between intermediate cover, regrowth, and/or weeds is not obvious. The composition of the cover crops is not taken into account for the moment, due to lack of information, but may be in the coming years depending on the data provided by the farmers.

In the current version of the SAFY-CO2 model, the estimates of organic matter evolution are only valid on soils depleted in organic matter, which is the case for the vast majority of agricultural plots. A thesis is underway for soil contexts richer in organic matter with the aim of having relevant parameters to enter into the model for these situations.

Several projects and initiatives are underway:

A heavier treatment chain, AgriCarbon-EO, is currently being deployed. This chain will make it possible to consider both Tier 1 and Tier 2 approaches, but also Tier 3 by integrating the SAFY-CO2 model. And the processing chain should be able to recover data sources from land management software, in particular from the Mes Parcelles software. A coupling between the AMG soil dynamics model (presented in the next section) and the SAFY-CO2 model could improve the estimation of organic matter decomposition in the soil. SAFY-CO2 currently only estimates it with a simple approach based on temperature levels. AMG, on the other hand, goes much further by integrating the chemical properties of the soil. The combination of the two models will make it possible to combine soil and biomass models to better estimate changes in soil carbon stocks. It should also be noted that, for the moment, AgriCarbon-EO does not take into account the nitrogen applied and its impact on greenhouse gases. Unlike the SAFY-CO2 model, which was initially oriented towards research, the developers of the AgriCarbon-EO processing chain have worked on propagating the uncertainties of the input data to the outputs of the treatments. No decotations are currently required by the CAP or any other mechanism depending on the accuracy of the model, but in a broader context, it is conceivable that this could become the case. The objective of this uncertainty propagation work is to quantify the uncertainty on each of the simulated variables (CO2 flux, yield, biomass, etc.) in order to produce uncertainty maps. The AgriCarbon-EO processing chain has been designed to be consistent with the MRV (monitoring, reporting, verification) strategy of the CAP, and is compatible with a low-carbon label method.

The AgriCarbon-EO chain is still a tool that is closer to the research domain. It is not yet operational, and the question of scaling it up, or in other words who will be in charge of managing the satellite data and using the AgriCarbon-EO chain, will arise. Could the ministry do this? Or perhaps the European Copernicus programme? Someone will have to step in to provide the service.

In the wake of COP21, the H2020 Circasa project has defined a methodology to address carbon footprints in a spatialised manner. The project ended a few months ago but a follow-up should be set up. Another H2020 project, the NIVA project, is still ongoing in 2021. NIVA aims to develop a nested approach with three levels of complexity – still following the Tier 1, Tier 2, and Tier 3 taxonomies – on carbon, nitrate leaching and biodiversity indicators. The Tier 1 level is based only on satellite data and the graphical parcel register (RPG). For the carbon balance maps at the plot level, a link is made between the duration of soil cover and the quantity of CO2 absorbed (the link was established on about twenty sites with flux exchange measurements by Eddy Covariance). The relationship is generic and can be applied to many crops (except rice). The objective is to produce maps, at the plot or pixel level, of areas that fix or not CO2, and to monitor plots close to equilibrium. The Tier 2 level still uses this empirical relationship between the duration of soil cover and the quantity of CO2 absorbed, but also integrates farmer data to achieve a more complete carbon balance by calculating the quantities of carbon exported at harvest (in grain, straw, fodder, etc.) or added in the form of amendments. Tier 3 is based on the SAFY-CO2 model described above.

The Quantica project focuses on the specific contribution of intercrops. The objective is to specifically measure the biomass of the cover crops with the aim of refining the carbon balance at the plot level: taking into account both what happens in crops and intercrops over one or more years. We are specifically interested in intercropping and the biomass of the cover crop to store carbon in the soil. The detection of intercropping works quite well to discriminate bare soil from covered soil. Radar data can even be used as a complement to compensate for the presence of clouds. Estimating biomass by radar is far from simple, as these signals are sensitive to soil moisture and water content (the company OneSoil already offers biomass maps interpolated with radar data). The most important thing is to have satellite images at the end of the growth of the canopy, as this is what will be buried in the soil. However, the question of the cover crop is not obvious, especially as these are often mixtures.

The AMG model

Developed by AgroTransfert and its partners, the AMG model is a dynamic soil model – it is therefore a Tier 3 model – which focuses on soil carbon storage and organic matter management. The model considers a set of simple input data to describe the farm (yields, intermediate cover, tillage, irrigation, etc.) and to estimate the carbon that will enter the soil through crop residues and be transformed into humus. By adding the type of soil and climatic data, it is possible to obtain a humified soil carbon balance. The output of the AMG model is the evolution over time of the carbon stocks and its content in the surface layers.

The AMG model could also be coupled with remote sensing data, as discussed in the previous section about SAFY-CO2. Classically in AMG or in other dynamic soil models, biomass is not measured but estimated, often from yield and allometric functions. This source of uncertainty could be reduced by measuring a biomass level from satellite imagery.

The AMG model is integrated into the Simeos-AMG tool, which is basically AMG with an interface. The software is made to help see what could be expected from new practices compared to a reference situation and to make a decision on the long term. The software is also used to make simulations and to project oneself (by asking for example if there would be interest in exporting straws, and if so at what rate…)

The AMG model was developed for vines in collaboration with IFV and INRAE. The mineralisation functions used are the same, only the model inputs change. Discussions are underway to implement the AMG model on grasslands.

The AMG model is also an integral part of the ABC’Terre method, the objective of which is to carry out a greenhouse gas balance on the scale of the territory, by integrating, among other things, the effects of carbon in soils thanks to the AMG model. The inputs to the AMG model are determined using relatively large data sources, in particular the graphical parcel register (RPG) to reconstitute rotations by soil type and farm, but also the soil analysis database (BDAT) set up by the Gis Sol. Understand that ABC’Terre uses the outputs of the AMG model, but is not exclusive to it. It also includes emission factors from the Agribalyse database and IPCC emission factors.

Cool Farm Tool

Originally developed by the University of Aberdeen, Unilever and the Sustainable Food Lab, Cool Farm Tool (CFT) is a tool for calculating the carbon footprint of farms, considering both emissions and soil carbon storage. The CFT considers Tier 1 and 2 for livestock (dairy and beef) and crops, as well as a “simple” Tier 3” model when it comes to N2O emissions and soil carbon sequestration. The tool is partly aligned with a number of standards and protocols (IPCC, GHG protocol…) but does not necessarily seek to be fully compliant. Even if some approaches are still rather simplistic – for example on plant cover – the tool continues to be improved regularly. Keep in mind that Cool Farm Tool is mainly referred to for its carbon aspects, but the tool also looks at water resources, nitrogen efficiency, and biodiversity.

The tool is relatively simple to use, with many default values (it is also possible to define ranges rather than single values), and the majority of the input data is filled in manually. The tool links to external databases, notably to retrieve climate data and water availability. Unlike other tools or models we have described, the tool does not use satellite data to calculate soil biomass or carbon levels. However, APIs would be available to work with a geospatial player, GeoFootPrint.

The Cool Farm Tool is not yet widely used in the carbon markets – it was initially a tool for decision support. Cool Farm Tool is still a measurement tool. It is not a certification tool and does not currently qualify a carbon credit. However, the Cool Farm Alliance is working to improve the tools’ structure and methodology so it becomes compatible with the variety of carbon crediting schemes globally. For carbon markets, the Cool Farm Tool is promoted by members such as the Danish company Commoditrader or the Belgian company Soil Capital, which considered that the tool enjoyed a sufficiently solid scientific and industrial consensus (many industrialists participated in its financing) to rely on it. Soil Capital is setting up carbon reward schemes for farmers, certified to ISO 14064 (an ISO standard for quantifying, monitoring and reporting greenhouse gas emission reductions or removal improvements), and the ISO certificates generated are sold by its partner South Pole.

The Verra VCS method

Verra has developed its own programme – VCS – describing a set of procedures for calculating greenhouse gas emission reductions. Specific methodologies are then developed for each activity and sector (industrial processes, construction, waste, transport, etc.). There are several methodologies specific to agriculture, including the SALM methodology (VM0017), and more recently, a more integrated and general methodology – IALM (VM0042). The proposed methodologies are reviewed by Verra, but also by independent third parties. A public consultation is also set up. VCS-labelled projects are also audited by a structure independent of Verra. The company is not involved in carbon credit transactions at all (Verra does not sell credits directly), as contracts are set up outside the VCS programme.

At the moment, the majority of VCS standardised projects are in the forestry context. Few projects are still oriented towards agriculture. The VCS standardised methodologies are currently very oriented towards soil sampling (revisions are underway to combine soil measurements and dynamic models), and are very rigorous on the verification and monitoring requirements

Identified limitations and weaknesses of existing tools

From a purely agronomic point of view, the subject of carbon is still the subject of much debate among the main stakeholders. Without getting into parochial disputes – and this blog post is not a scientific article – let’s quickly review the main points of attention raised by the community (the points are not exhaustive). The aim here is not to provide a clear answer but rather to raise a number of questions:

- Progress seems necessary to better simulate the evolution of the carbon stock in deep horizons and in particular to take into account new mechanisms such as the “rhizospheric priming effect”. Roots produce thousands of exudates depending on the context in which the plant is located. In soil that is stuck to the roots – known as rhizospheric soil – carbon could be mineralised 2 to 3 times faster. In current models, the quantity of carbon returned by the soil could therefore be underestimated. This priming effect could also lead to a revision of the coefficients of mineralisation in soils.

- Some people criticise the long-term experimental data used in the carbon estimation models for lacking completeness, with too few soil types and textures considered. Results from experimental stations are sometimes criticised for being in contradiction with results in the field from pioneer farmers (not the same agri-equipment [seeders…], not the same working methods…). More specifically, the French carbon estimation models would not be calibrated for high biomass plant cover crops (whose quantity of carbon stored would then be largely underestimated). Some of the tools currently proposed would nevertheless make it possible to overcome this problem by artificially multiplying the frequency of crop returns. Other criticisms relate to the fact that direct seeding under cover would not be considered (direct seeding alone is). The plant cover used would also not be deep enough to store organic matter in depth (lack of soil compaction management). Organic matter profiles in grasslands would not be deep in the sense that they are cut all the time (or grazed)

- The effect of no-till on soil carbon storage/removal is still a hotly debated topic. The latest INRAE report and recent meta-analyses suggest that no-till has no effect on the total amount of carbon stored, as the carbon is distributed over the entire vertical soil profile. Opponents criticise the experimental data for having been studied by considering each agricultural practice (stopping ploughing, introducing cover crops, etc.) independently, whereas these practices would have significant combined effects. The latter add that the effect of no-tillage would be all the more important as the soils are already very rich in organic matter.

- Certain agricultural practices, notably fertilisation and irrigation, would be in opposition to the storage of carbon in the soil. Fertilisation and irrigation would increase the mineralisation of carbon. There would therefore be a balance to be struck between fertilisation and yield levels so as not to encourage the removal of carbon. This dilemma could particularly affect farms undergoing organic conversion which, if they do not use strong intercropping, could be led to destock carbon by adding nitrogenous fertilisers. Nitrogen fertiliser seems to be necessary at the beginning to reach the self-fertilising state mentioned above.

- There would also appear to be a trade-off between soil carbon storage and nitrous oxide emissions.

- One of the main levers for reducing greenhouse gases – reducing the number of animals on the livestock farm – would not be taken into account in some of the methods for scoping greenhouse gas emission reductions.

Some additional information

- INRAE and Planet-A are developing the SOCCROP indicator to monitor the evolution of carbon stock in agricultural soils

- The organisation PADV (for a living agriculture) is working on a farm regeneration index. This index is not specific to carbon.

- Some actors to follow on the subject of carbon: MyEasy Farm, Soil Capital, AgroTransfer, Carbone Farmers, Rize Ag, Indigo, Nori, Truterra, Climate Action Reserve, TerraCarbon…

- Some information on carbon standards

A carbon market that is being set up

The main principles of carbon payout

Carbon markets are subject to a number of key principles that must be kept in mind to ensure that a euro spent really does go towards a project that has an impact:

- Additionality: To demonstrate the additionality of a carbon project, one must be able to prove that this carbon project could not have taken place without the proposed aid and/or financing. In other words, it must be shown that this project goes beyond the conventional trend, beyond what would have been done naturally, or beyond what the regulations would have imposed anyway. If the farmer or other beneficiary of the project has their own funding, there is no reason why they should get carbon funding as they could have somehow set up the project on their own.

- Double counting: It is necessary to ensure that a GHG emission reduction or carbon storage action implemented as part of a carbon project is not counted or paid for twice for the price of one. This principle of double counting will become increasingly important because there will be more and more offsets and schemes put in place. A concrete example: An agricultural cooperative is ensuring that its members develop a low-GHG sector. Who gets the carbon credits? To the members who have reduced their footprint? To the cooperative? Or perhaps to the downstream distributor who has imposed a low-GHG product? And if a member has several low-GHG sectors, how can the carbon count of the actions he or she has implemented for these sectors be shared, knowing that certain global actions on his or her farm will have served both sectors? We could already allow this member to exclude the emissions of one of these crops, but we would not be completely out of the woods. How does an agribusiness trade with another industry if one of them wants to finance a low carbon project? Should we separate emission reductions from carbon storage? Do the stored credits belong to the agribusinesses? If an agribusiness finances a farmer and the latter wants to make even more effort, should new credits be generated? In short, an accounting puzzle that is far from being completely resolved. In agriculture, this issue is extremely complicated because the sector is multi-subsidised, and there are many players. As the sector feeds several markets, all of which will (have to) share emission allocations, the task will be far from easy. Add to this the fact that if there were only one counting method, it would be fairly straightforward. But when several methods are put in place – we can take the example of the Label Bas Carbone (LBC) for livestock, field crops or methanisation – it becomes much more complicated. Note, for example, that the Carbon Agri method will soon be updated to include the LBC method for field crops. To reassure ourselves a little, there are some reduction/storage methods that do not overlap too much either, and that will allow us in some cases not to get our brains in knots (for example between the Carbocage project on hedges and the low carbon label for arable crops).

- Permanence or non-reversibility: it is all very well to implement an action to reduce emissions or store carbon, but it must be sustainable over time! The first example is a fairly simple forestry project where I plant a tree. When this tree grows, apart from the fact that it is cut down, burnt or diseased (that’s quite a lot, you might say), the carbon storage is sustainable. In agriculture, it’s a bit more complicated than that because the storage comes from the fact that the farmer is going to put in place practices. But if five years later, either because he’s fed up, or because he sells his farm, or for any other number of good reasons, he re-emits the carbon he helped store, the permanence of the credit is no longer guaranteed… Some methods impose mandatory discounts to take into account these aspects of non-permanence or non-reversibility; we’ll come back to this a little later.

All these major principles directly or indirectly entail a need for traceability of both the action and the financing of the action. Many methods impose strict conditions for auditing and verifying projects, and this is done in a totally independent manner by third-party auditors. Information and investment must be tracked. It is also important to work at the system or farm level. Working on a crop-by-crop basis certainly seems more attractive because of its simplicity – it is relatively easy to find relevant environmental monitoring indicators – but the approach is not very robust to side effects and cross-crop impacts.

Carbon markets

The bond markets under the Kyoto Protocol

In 2005, following the Kyoto Protocol, three main carbon markets emerged:

- An Emissions Trading Scheme (ETS). You may have seen the acronym EU-ETS, which is in fact nothing more than the European Emissions Trading Scheme. Keep in mind that many countries or groups of countries have set up emissions trading systems (Europe, China, Korea, Switzerland…) but that these different systems of allowances are hermetic (for the moment, it is not possible to trade allowances between different systems). The European Emissions Trading Scheme has been broken down into several phases over time (the 3rd phase runs from 2013 to 2020 and the 4th phase from 2021 to 2030). This system was set up to encourage the most polluting companies (energy-intensive industries, electricity producers, etc.) to reduce their greenhouse gas emissions and limit their carbon footprint. An emissions quota (what they are allowed to emit at the most), called EUA for European Allowances, is then set by sector. Companies can resell allowances if they have emitted less than they were allocated, or buy them if they have emitted more than expected. The idea is to progressively reduce the ceiling of EUAs distributed so that companies emit less and less. In the European market, the reduction target for 2020 compared to 1990 was 20%.

- A joint implementation mechanism (JI). In this JI market, industrialised countries, i.e. the Annex I countries of the Kyoto Protocol (see the first section of this article), have the right to buy emission reductions from other industrialised countries through ERUs (emission reduction units) generated by JI projects.

- A Clean Development Mechanism (CDM). The principle of the CDM market is the same as the JI market, with the major exception that an industrialised country buys emission reductions from emerging or developing countries (countries that are not in Annex I of the Kyoto Protocol), and not from other industrialised countries. The credits generated by CDM projects are called CERs (certified emission reductions). The aim was to give industrialised countries the opportunity to finance projects in southern countries and reduce their emissions there. The idea was that the constraints and costs of reducing greenhouse gas emissions in the South would be lower than if these emission reductions had been implemented in an industrialised country. This clean development mechanism (CDM) is nevertheless widely criticised for the uncertainties surrounding the additionality of projects, the sectoral and geographical distribution of projects, and the governance and ethics of the projects implemented (Demaze, 2013).

Carbon credits can be traded between players (buyers and sellers) either on marketplaces, directly or via an intermediary, or over the counter. These three markets, the ETS, JI and CDM, are considered to be carbon bond (or regulated) markets in the sense that states and companies are subject to emission reduction targets and constraints. As you may have already realised, these three markets are quite different, apart from the fact that each one involves accounting for tonnes of CO2 equivalent. In an emissions trading scheme, companies and countries trade emission allowances (okay, we’re not that far along…). These emission allowances (we have talked about EUA : European Allowances) are in a way rights to pollute. But you have to realise that they are rights to pollute in the future. On the contrary, in the JI and CDM markets, countries and companies buy emission reduction credits (ERUs or CERs) which are in fact offsets for emissions that have already taken place. They are therefore not rights to pollute in the future but compensation in the past.

The EU ETS only applies to the most polluting sectors. Not all sectors are subject to it and therefore do not have the same objectives and regulations to respect. In addition to the EU-ETS, there are two other climate policies for Europe:

- The effort sharing policy, referred to by the acronym ESD (Effort Sharing Decision) over the period 2013-2020, then ESR (Effort Sharing Regulation) for the period 2021-2030. The sectors subject to this effort sharing (transport, construction, agriculture, waste) are subject to annual emissions caps, expressed as a percentage of 2005 emissions. By 2030, emissions from these sectors must be reduced by 30%.

- Land use, land-use change and forestry (LULUCF), which are changes in soil and forest carbon stocks. LULUCF is currently the only sector that allows for negative emissions thanks to natural carbon sinks: biomass (forests, hedges, agroforestry, etc.) and soils (agricultural soils, etc.).

The European objectives are then broken down in each country, which then break them down by sector. Each company in its sector (ETS, ESR or LULUCF) therefore has different reduction targets to meet. However, a number of flexibility mechanisms have been put in place to help countries and companies meet their targets. For example, it is possible to carry over credits from one period to another: emissions trading schemes have been defined over several different periods – it would then be possible to carry over a credit from, say, the 2013-2020 period to 2021-2030. By deferring a credit, one abstracts oneself from the obligation to repay one’s carbon debt at a given moment, and assumes that one will reduce it later. It would even be possible in some cases to finance credits from one sector with credits from another. For example, it would be possible to finance the credits of the ESR sector with those of the ETS or LULUCF sector. In principle, there might be no problem with this, except that some of these sectors are or have been heavily over-credited (and not necessarily for the right reasons, as we will discuss later), which means that it is quite easy to move credits between sectors and not engage in a low carbon transition. Each trading scheme manages how credits can be used. CERs (CDM projects) or ERUs (JI projects) can, for example, be used to meet part of the obligations that countries may have under a trading scheme (an AAU will then have to be cancelled to generate an ERU so as not to double-count emissions reductions). In addition, it would appear that the European Commission is setting emission reduction starting points theoretically higher than they actually are, making it all the easier to meet targets.

The price of carbon credits on the bond market has fluctuated quite significantly (see Figure 8), for several reasons. The first is that a number of emission allowances in the ETS were allocated for free. If you look at it that way, you might think it’s a scandal, because if you sell allowances for free, how can you expect companies to reduce their emissions on their own? In Europe, the explanation lay in the fact that credits allocated free of charge to European companies could avoid penalising European industry in relation to its competitors, and avoid carbon leakage. The second important reason was that on the one hand the initial reduction targets of the Kyoto Protocol were quite low and therefore easily achievable, and on the other hand the economic crisis of 2008-2009 naturally led to a decrease in carbon emissions in a number of countries. As a result, companies had a lot of allowances to sell and the price of allowances collapsed, simply by following the principle of supply and demand. The price of these carbon allowances fell to a few euros, and remained very low until recently (Figure 8). To raise the price of carbon, two mechanisms were put in place a few years ago: a mechanism for purchasing allowances at auction and a market stability reserve mechanism. The reserve mechanism makes it possible to remove excess allowances from the market (and artificially reduce the supply of credits, thus raising prices), and to potentially put them back on the market later. Could we also imagine a floor price for carbon to avoid these pitfalls?

Figure 8. Carbon price changes in the EU-ETS market. EUA stands for European Allowances

The governance of the ETS as presented above has been established until 2018. The fourth phase of the ETS (2021-2030) is expected to initiate a number of changes. The cap on distributed allowances will continue to fall, but at a greater rate than before (from 1.74% per year to 2.2%). The allowances allocated so far for free will continue to be allocated over this new ten-year period, mainly to those sectors most exposed to the risk of relocating their production outside the European Union. Sectors that are less exposed to the risk of relocation will see their free allowances decrease, until they are definitively eliminated in 2030, at the end of phase 4 of the ETS. In view of these fairly strong constraints on the reduction of free allocations of allowances since the Paris Agreement, the investment kinetics are weaker than this regulation. The demand for allowances becomes high and as the supply is low, the price of carbon rises – still following the classic paradigm of supply and demand. In the bond market, the tonne of carbon is currently around 60 euros. Again, keep in mind that the agriculture sector is not included in the ETS, the objective being to force companies under quota to reduce by themselves by investing on their carbon impact.

The CDM projects should have seen their days over at the beginning of 2021, i.e. at the end of the second application period of the Kyoto Protocol. I remind you that the Paris Agreement is supposed to have taken over from the Kyoto Protocol on 1 January 2021. It was initially decided that CDM projects would be transformed into SDM projects [Sustainable Development Mechanisms) (in general, when you start hearing about sustainable development, it doesn’t smell very good…). So a few questions arose: What are we going to do with the CDM projects already underway? Should they be maintained or cancelled? How to transfer credits from CDM projects to SDM projects? How do we properly account for the credits to ensure that they are not counted twice, both for the country financing the project and the country implementing the project at home? Or in other words, how to account for CERs. It is important to understand that before the Paris Agreement, under the Kyoto Protocol, some countries had committed to reducing their emissions (Annex I countries) while other so-called non-industrialised countries (non-Annex I countries) had not. CDM projects then allowed Annex I countries to finance projects in non-Annex I countries. With the Paris Agreement, as all countries have committed to emission reductions, the principle of CDM projects no longer makes sense. The last COPs (Nos. 24 and 25) did not lead to a clear consensus on what should be done with these CDM projects. COP26 is expected to resolve this issue. A provisional consensus has nevertheless been reached: CDM project applications from 1 January 2021 onwards will still be registered but their approval will be provisional. They will only be definitively accepted if, at the end of COP-26, it is decided that the CDM mechanism is maintained.

The voluntary markets under the Kyoto Protocol

Quite intuitively, voluntary markets are different from bond markets in that countries or companies commit to emissions reductions without being bound by a particular regulatory framework. These markets therefore allow those who are not subject to the emissions trading scheme to participate in carbon trading as well. However, the total credits generated in voluntary markets remain much lower than those generated in regulated markets.

A number of voluntary certification frameworks – such as the Label Bas Carbone – are being set up. I would like to stress that voluntary certification frameworks should not be confused with a taxation system, they are two different things (we will discuss this later). In the framework of voluntary certification, credits are generated by mutual agreement and a relationship is built between an investor (the one who buys carbon credits), a project leader or agent (the one who organises, facilitates and coordinates a low-carbon project) and an implementer (the one who sets up the project, often an agricultural player in our case).

Two examples will perhaps be more telling:

- The company Soil Capital positions itself as a project developer, between farmers and buyers of carbon credits. Soil Capital approaches farmers, calculates the potential for carbon credits using the Cool Farm Tool, certifies the credits with its partner South Pole (an expert in carbon remuneration), which then sells the credits generated to private companies that want to buy carbon credits. Soil Capital buys the credits at €27 (farmers are therefore paid €27 per tonne of carbon) and sells them, via its partner South Pole, at around €40 to credit buyers.

- The France Carbon Agri association aims to facilitate the implementation of the Carbon Agri method. The association organises calls for projects so that producer groups (producer associations, cooperatives, etc.) can support producer projects during the period of labelling. France Carbon Agri trains and supports the use of the Carbon Agri method and the Cap’2ER tool, and ensures the certification of projects via the certifier Bureau Véritas. France Carbon Agri also sells the carbon credits generated. These credits are currently sold at €38 per tonne of carbon, of which €30 goes to the farmers.

Is it then possible to create fungibility or a strong link between the bond and voluntary markets? This is obviously under consideration. The problem of double counting is still prevalent. Let’s take the example of starch producers or maltsters who are under quota because of their energy-intensive factories, but who are also supplied by the agricultural sector. Their impact therefore also comes from agriculture (and this is notably the case for most of their Scope 3). Nevertheless, one may wonder whether opening up bond credits to the voluntary market will not add significant complexity to the systems in place, and make it even more difficult to set up projects and/or access carbon credits. As we shall see shortly, there are many possible financing mechanisms within the framework of the voluntary market, and these mechanisms may be sufficient in themselves.

How are carbon markets evolving in the wake of COP26?

COP26 in Glasgow took place in October 2021. It was an opportunity to discuss Article 6 of the Paris Agreements, which mainly deals with the way in which emission reductions will be accounted for (the establishment of carbon credit markets and trading mechanisms)

In order not to clutter up this already long blog post, I have written a special one on the feedback from COP 26. I invite you to read this complementing dossier

Ancillary financing methods

The voluntary certification framework is interesting, of course, but it must be borne in mind that it is an independent auditor who will generate credits and then sell them, and this within a relatively long period of time, 5 years or more. We can therefore imagine many other mechanisms in place to avoid putting everything on the farmer.

Tax

One of the first things we can think of is the tax! There are so many different ones, why not put one on carbon? And we could, for example, use the money from this tax to finance projects with a high environmental impact. Today, there is a tax on petroleum products and agriculture is exempt. It was proposed very recently to raise this tax on fuels, and everyone knows what happened in France… Little hint, it’s yellow. The fuel tax was subsequently frozen at €44. It seems for the moment that we can forget about the solution on taxation

Aid – State intervention